TL;DR:

- Mortgage origination involves all steps from application to closing, impacting rates and costs.

- Using wholesale brokers can lower fees and rates through lender competition.

- Being informed and assertive in negotiations helps first-time buyers save on origination costs.

Most first-time buyers think mortgage origination is just a pile of paperwork standing between them and their new home. It's not. Origination is the entire process of creating your home loan, and every step inside it directly shapes your interest rate, monthly payment, and how fast you close. The difference between a buyer who understands origination and one who doesn't can be thousands of dollars over the life of a loan. In 2025, average origination costs ran around $11,800 per retail loan. This guide breaks down every stage, every player, and how to use wholesale broker access to work the system in your favor.

Table of Contents

- What is mortgage origination?

- Steps in the mortgage origination process

- Wholesale vs. retail mortgage origination: Which should you choose?

- How origination costs, rates, and trends affect first-time buyers

- What most first-time buyers miss about mortgage origination

- Find your best mortgage origination option with expert help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand origination basics | Learning what mortgage origination means helps you avoid costly mistakes and delays. |

| Compare wholesale vs retail | Exploring both options empowers you to find better rates and lower fees. |

| Watch for hidden fees | Ask for transparent fee breakdowns up front to prevent sticker shock at closing. |

| Leverage broker competition | Negotiating with brokers and lenders often leads to better terms for first-time buyers. |

| Prepare documentation early | Gather all paperwork ahead of time for a faster, smoother origination process. |

What is mortgage origination?

Mortgage origination is the full sequence of steps that turns your home loan application into a funded mortgage. It starts the moment you apply and ends when you sign at closing. Think of it as the assembly line for your loan. Every station on that line, from your application to the final approval, adds something to the finished product.

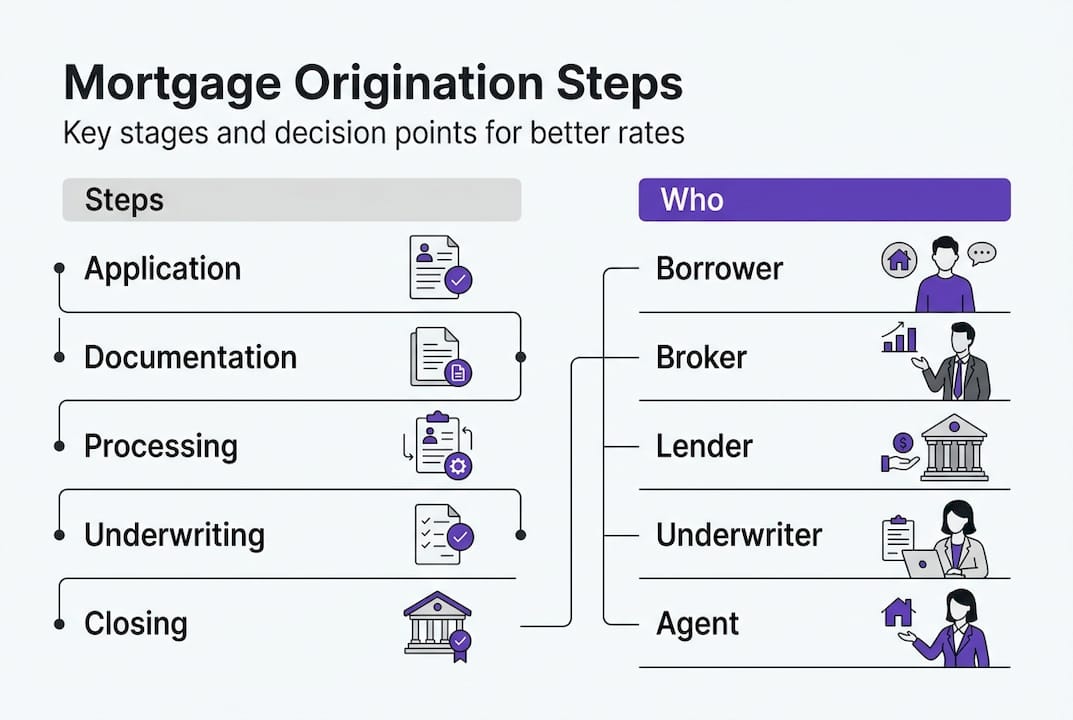

Three main players are involved:

- The borrower (you): You supply the financial information, sign documents, and make decisions.

- The lender: The institution that ultimately funds the loan, whether a bank, credit union, or wholesale lender.

- The broker (if you use one): A licensed professional who shops multiple lenders on your behalf to find the best rate and terms.

A few key terms are worth knowing before you go further. The origination fee is a charge the lender or broker collects for processing your loan, usually expressed as a percentage of the loan amount. Underwriting is the risk review stage where a lender decides whether you qualify. Wholesale origination means a broker sources your loan from a lender who doesn't deal directly with the public, often unlocking better pricing. Retail origination means you go straight to a bank or lender and work entirely within their product lineup.

Why does this matter for first-time buyers? Because the channel you use to originate your loan affects your rate, your fees, and how long the process takes. A retail lender can only offer you their own rates. A wholesale broker can shop dozens of lenders and present you with competing options. That competition is what drives your cost down.

When you start exploring mortgage qualification steps, origination is already in motion. Even mortgage pre-approval is part of the origination chain. Understanding where you are in the process helps you ask better questions and make smarter decisions.

Pro Tip: Before you commit to any lender or broker, ask for a written, itemized breakdown of all origination fees. Compare line by line, not just the headline rate.

Steps in the mortgage origination process

Knowing the stages of origination helps you anticipate what comes next and avoid the mistakes that slow things down. The average process takes 30 to 45 days, but that timeline can stretch or shrink depending on how prepared you are.

Here are the six core stages:

- Application: You submit your loan application with basic financial details, including income, assets, and the property address.

- Documentation: You provide supporting documents such as tax returns, pay stubs, bank statements, and ID.

- Processing: A loan processor organizes your file, orders the appraisal, and verifies your information before sending it to underwriting.

- Underwriting: An underwriter reviews your full financial profile and the property's appraisal to assess risk and confirm you qualify.

- Approval: You receive a conditional or final approval. Conditions might include updated pay stubs or a letter explaining a credit inquiry.

- Closing: You sign the final loan documents, pay closing costs, and receive the keys.

Here's a rough timeline for each stage:

| Stage | Estimated time |

|---|---|

| Application | 1 to 2 days |

| Documentation | 3 to 7 days |

| Processing | 5 to 10 days |

| Underwriting | 7 to 14 days |

| Approval | 1 to 3 days |

| Closing | 1 to 3 days |

The most common delays happen during documentation and underwriting. Missing a bank statement, having an unexplained deposit, or waiting on a slow appraiser can add days or even weeks. You can see a helpful visual overview in this pre-approval infographic that maps the early stages clearly.

If you want to move fast, start getting pre-approved before you find a property. That way, your documentation is already verified and underwriting has a head start. Also, shopping for the best rate early gives you leverage when comparing lenders.

Pro Tip: Gather every document your lender requests within 24 hours. Every day you delay is a day added to your closing timeline.

Wholesale vs. retail mortgage origination: Which should you choose?

This is the decision most first-time buyers don't even know they're making. When you walk into your bank and apply for a mortgage, you've already chosen retail origination. When you work with a licensed mortgage broker, you're accessing wholesale origination. The difference is significant.

With retail origination, the lender handles everything in-house. You get convenience and a single point of contact, but you're limited to that lender's products and pricing. There's no competition working in your favor.

With wholesale origination, a broker acts as your advocate. They submit your file to multiple wholesale lenders who compete for your loan. That competition typically produces lower rates and fees. In 2025, retail origination averaged $11,800 per loan, while wholesale options often came in noticeably lower.

Here's how the two channels compare:

| Feature | Wholesale | Retail |

|---|---|---|

| Rate options | Multiple lenders | Single lender |

| Origination fees | Often lower | Typically higher |

| Flexibility | High | Limited |

| Speed | Varies by broker | Typically standardized |

| Personal guidance | Strong (broker advocacy) | Moderate |

Factors to consider when choosing:

- Rate priority: If getting the lowest possible rate matters most, wholesale wins.

- Simplicity: If you want one institution handling everything and rate is secondary, retail may suit you.

- Loan complexity: Self-employed buyers or those with non-standard income often benefit more from wholesale access.

- Time: A well-organized broker can close as fast as a retail lender.

The broader market reflects this shift. Q3 2025 origination volume reached 1.77 million loans totaling $600 billion, down 2% quarter-over-quarter, signaling that buyers are being more selective. Understanding how mortgage rate impacts ripple through your payment helps frame this choice clearly.

For deeper guidance on navigating this, explore wholesale lender shopping and how competitive mortgage rates through brokers can translate into real savings.

How origination costs, rates, and trends affect first-time buyers

Origination costs are not a single number. They're a collection of charges that add up quickly if you're not paying attention. The main components include the lender origination fee, discount points (optional prepaid interest to lower your rate), appraisal fees, credit report fees, and title-related charges.

Understanding each line item gives you negotiating power. Some fees are fixed. Others are not. Broker fees, for example, are often negotiable, especially when multiple lenders are competing for your loan.

"In Q3 2025, U.S. mortgage origination totaled $600 billion across 1.77 million loans, reflecting a market where buyers who compare options hold real leverage." Q3 2025 loan origination report

In 2026, a few market trends are worth watching. Rates remain sensitive to Federal Reserve policy signals. When loan volume drops, lenders compete harder for business, which can work in your favor. Staying informed about mortgage rate trends helps you time your application more strategically.

Here's how to reduce what you pay at origination:

- Request loan estimates from at least three lenders or brokers and compare every fee line.

- Ask specifically which fees are negotiable. Many buyers never ask.

- Consider whether buying discount points makes sense based on how long you plan to stay in the home.

- Work with a broker who has access to lender competition across multiple wholesale sources.

- Review the mortgage trend benefits that can also apply to buyers in a shifting rate environment.

Pro Tip: When a broker knows you're comparing them against two other brokers, they have a real incentive to sharpen their pricing. Use that leverage openly and without apology.

What most first-time buyers miss about mortgage origination

Here's the part most guides skip: mortgage origination is a negotiation, not just a process. Every fee, every rate, and every timeline is influenced by how informed and assertive you are as a borrower.

Most first-time buyers treat origination like a form they have to fill out correctly. They focus on not making mistakes rather than on extracting value. That's the wrong mindset. The buyers who get the best outcomes treat every stage as an opportunity to ask questions, push back on fees, and compare options side by side.

Strong documentation isn't just about avoiding delays. It signals to lenders that you're a low-risk, organized borrower, and that can subtly influence how aggressively they price your loan. A broker who sees a clean, complete file is also more motivated to go to bat for you.

First-time buyers often feel intimidated about asking for better terms. Don't be. Lenders expect negotiation. Brokers are paid to advocate for you. Understanding mortgage compliance tips also helps you recognize when a fee structure is out of line. The more you know, the harder it is for anyone to overcharge you.

Find your best mortgage origination option with expert help

Now that you understand how origination works and where the real opportunities are, the next step is connecting with someone who can act on that knowledge for you.

LoFiRate.com's broker matching services connect you with licensed wholesale mortgage brokers in your state who shop multiple lenders to find competitive rates and lower origination fees. You're not locked into one lender's pricing. You get real options, real comparisons, and a professional working on your behalf. Explore the available loan options and request a no-obligation consultation today. There's no cost to compare, and the savings can be substantial.

Frequently asked questions

How long does mortgage origination take on average in 2026?

Mortgage origination typically takes 30 to 45 days, with delays possible based on documentation completeness and appraisal speed.

What are the main fees included in mortgage origination?

Origination fees cover lender charges, broker fees, and processing costs. In 2025, retail origination fees averaged $11,800 per loan.

What's the difference between a wholesale and retail mortgage?

Wholesale mortgages are arranged through brokers who shop multiple lenders, while retail mortgages come directly from a single lender with no external price competition.

How can first-time buyers reduce their mortgage origination costs?

By comparing offers from multiple lenders and negotiating broker fees directly, buyers can meaningfully lower what they pay at origination without sacrificing service quality.