TL;DR:

- A mortgage yield spread premium is lender-paid compensation to a broker for placing a loan above the par rate, which can lower closing costs. Regulatory rules now require full disclosure, making YSPs legitimate pricing tools rather than predatory practices. Borrowers should compare offers, understand break-even points, and ask brokers for the par rate to make informed decisions.

A mortgage yield spread premium (YSP) is lender-paid compensation to a mortgage broker for placing your loan at an interest rate above the lender's par rate. The par rate is the baseline rate at which the lender breaks even with zero points or credits. When a broker places your loan above that rate, the lender pays a premium to the broker. That premium can be passed to you as a credit toward closing costs, or it can stay with the broker as compensation. Understanding this mechanic protects you from paying more than necessary over the life of your loan.

What is mortgage yield spread premium and how does it work?

A yield spread premium functions as a pricing lever between your interest rate and your upfront costs. The higher your rate sits above the par rate, the larger the credit the lender generates. That credit can offset origination fees, title costs, appraisal fees, or other closing expenses.

The math is straightforward. For every 0.375% increase in interest rate above par, a lender typically provides a credit equal to roughly 1.00% of the loan amount. On a $400,000 loan, that means a rate 0.375% above par generates approximately $4,000 in lender credits. Those credits reduce what you pay at the closing table.

Mortgage brokers receive compensation either through borrower-paid fees or lender-paid YSP credits, but never both on the same loan. This rule keeps the compensation structure clean and prevents double-dipping. The structure affects how your loan is priced and how transparent the total cost appears on paper.

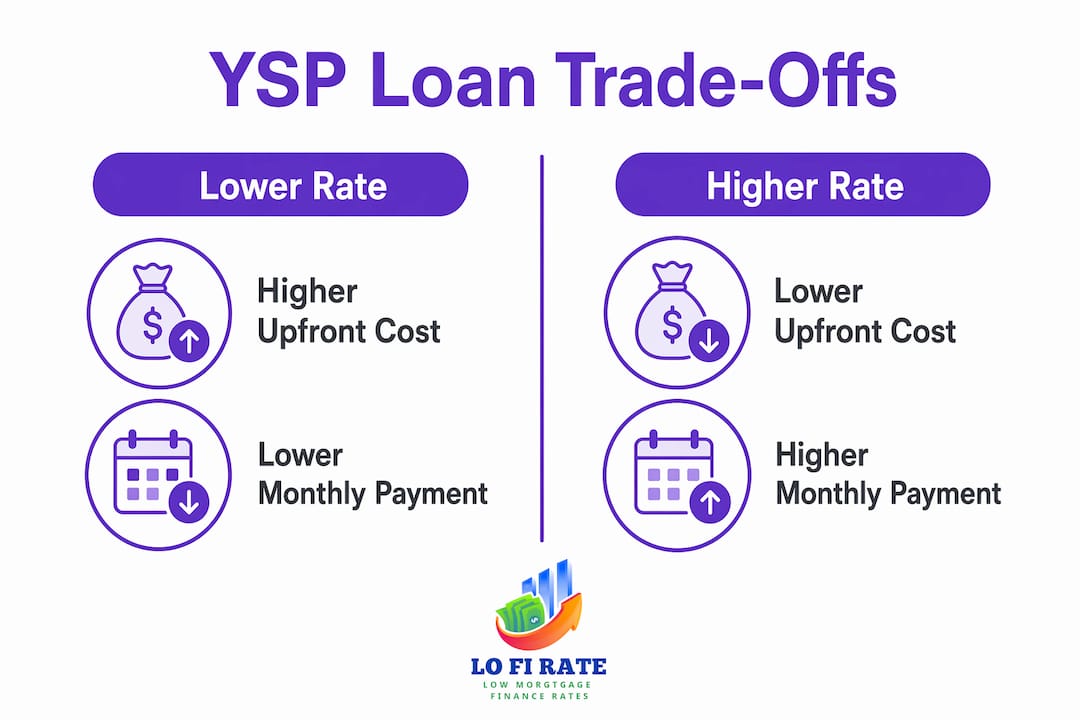

The trade-off is real. A lower rate costs more upfront. A higher rate costs less upfront but more over time. The table below shows how this plays out on a $400,000 loan.

| Scenario | Interest Rate | Lender Credit | Upfront Cost | Monthly Payment |

|---|---|---|---|---|

| Low rate, pay fees | 6.50% | $0 | $8,000 | $2,528 |

| Mid rate, partial credit | 6.875% | $4,000 | $4,000 | $2,627 |

| Higher rate, no-cost loan | 7.25% | $8,000 | $0 | $2,728 |

Note: Monthly payments are approximate and for illustration only. Actual figures depend on loan terms, taxes, and insurance.

Pro Tip: Ask your broker to show you the par rate in writing before agreeing to any loan. That one number lets you calculate exactly how much the rate spread is costing you over time.

How does regulation protect you from hidden YSP costs?

The regulatory environment around yield spread premiums changed dramatically after the 2008 financial crisis. Before that, brokers could steer borrowers into higher-rate loans without clear disclosure, collecting larger premiums without the borrower's knowledge. That practice ended.

The Dodd-Frank Act mandates full disclosure of all lender-paid broker compensation on both the Loan Estimate and the Closing Disclosure forms. These are the two documents you receive at the start and end of every mortgage transaction. Every dollar of broker compensation must appear on those forms.

Key protections you have today:

- Loan Estimate disclosure: You receive this within three business days of applying. It shows all fees and any lender credits tied to your rate.

- Closing Disclosure: Delivered at least three business days before closing, it confirms final numbers including broker compensation.

- Anti-Steering rules: Under the TRID disclosures and Anti-Steering rules, brokers cannot steer you toward a loan simply because it pays them more.

- No dual compensation: Brokers cannot collect both a borrower-paid fee and a lender-paid YSP on the same transaction.

- Post-Dodd-Frank compensation rules: Broker compensation cannot depend on loan terms like interest rate, which removes the incentive to push you into a higher rate for personal gain.

These rules mean that a disclosed YSP is not predatory. It is a legitimate pricing tool. The danger was always in the lack of disclosure, not the mechanism itself.

Pro Tip: Before closing, compare the lender credits on your Closing Disclosure to what appeared on your original Loan Estimate. If the numbers shifted without explanation, ask your broker directly. You can learn more about broker compensation rules and what disclosures to expect.

What are the real pros and cons of a YSP loan?

Accepting a loan with a yield spread premium built in is not automatically a bad decision. The right choice depends on your financial situation, how long you plan to stay in the home, and how much cash you have available at closing.

The advantages are concrete:

- You reduce or eliminate out-of-pocket closing costs, which can run $8,000–$15,000 on a typical home purchase.

- You preserve cash for reserves, renovations, or investments.

- Real estate investors sometimes use higher-rate loans strategically to protect cash flow on short-term property holdings.

- If you plan to sell or refinance within three to five years, you may never reach the break-even point where the higher rate costs more than the upfront savings.

The disadvantages are equally real:

A higher rate financed over the loan's full life can exceed upfront savings in just a few years. On a 30-year mortgage, even a 0.375% rate increase adds tens of thousands of dollars in total interest paid.

The break-even calculation is the tool that makes this decision clear. Divide the upfront savings by the monthly payment increase. If your closing cost credit saves you $4,000 and your monthly payment rises by $99, your break-even point is roughly 40 months. Stay past that point and the higher rate costs you more than you saved.

Borrowers commonly overlook this break-even math entirely, which leads to loans that cost far more than expected. Running the numbers takes ten minutes and can save you thousands.

How do you evaluate mortgage offers involving yield spread premiums?

Comparing mortgage offers is the single most effective way to avoid overpaying. Most borrowers accept the first offer they receive. That is a costly habit.

Here is how to evaluate any offer that involves rate credits or yield spread pricing:

- Request the par rate in writing. Knowing the par rate lets you benchmark every offer against the true baseline. Without it, you are comparing numbers without context.

- Compare Loan Estimates side by side. The Loan Estimate is standardized, which makes comparison straightforward. Look at the interest rate, lender credits, origination charges, and APR together.

- Calculate the break-even point for each offer. Divide the credit amount by the monthly payment difference to find how long it takes for the higher rate to cost more than you saved.

- Ask about transparent mortgage pricing. A good broker will walk you through the rate-versus-cost trade-off without hesitation.

- Get at least three offers. Wholesale brokers who shop multiple lenders give you access to a wider range of pricing than a single retail bank can offer.

The table below compares what to look for when evaluating two competing offers:

| Evaluation Factor | What to Look For | Red Flag |

|---|---|---|

| Par rate disclosure | Broker states it clearly in writing | Broker refuses or deflects |

| Lender credit amount | Matches Loan Estimate and Closing Disclosure | Credits shrink without explanation |

| Broker compensation | Disclosed on Loan Estimate | Not visible on any document |

| Break-even timeline | Under your expected time in the home | Exceeds five to seven years |

| APR vs. interest rate | APR accounts for all fees | Large gap between the two |

Questions worth asking your broker directly include: What is the par rate today? How much of this credit goes to your compensation versus my closing costs? What does this loan cost me if I stay for ten years versus five?

Is the yield spread premium still relevant in 2026?

The term "yield spread premium" is largely a legacy phrase. Most lenders and brokers today use the term "lender credits" instead. The concept, however, is identical. YSP terminology is legacy, but the pricing structure persists through lender credits with enforced transparency since the 2008 financial crisis.

The shift in language reflects regulatory cleanup, not a change in how mortgage pricing actually works. You still trade a higher rate for lower upfront costs. Brokers still receive compensation tied to that rate spread. The difference is that every dollar must now appear on your disclosure documents.

In 2026, with mortgage rates elevated compared to the historic lows of 2020 and 2021, the rate-versus-cost trade-off carries more weight. A 0.375% rate difference on a $500,000 loan is not trivial. Over 30 years, it represents a significant sum. Borrower education on this topic is not optional. It is the difference between a loan that fits your financial plan and one that quietly drains it.

Brokered loans give you access to multiple lender pricing sheets, which means you can compare par rates and lender credit structures across several institutions at once. That access is the practical advantage of working with a wholesale broker rather than a single retail bank.

Key takeaways

A yield spread premium is lender-paid broker compensation for loans priced above par, and understanding it requires comparing the par rate, lender credits, and break-even timeline before signing anything.

| Point | Details |

|---|---|

| YSP definition | Lender pays broker for placing your loan above the par rate, often as a closing cost credit. |

| Rate-credit trade-off | A 0.375% rate increase above par typically generates a 1.00% loan amount credit toward closing costs. |

| Regulatory protection | Dodd-Frank and TRID rules require full disclosure of all broker compensation on Loan Estimate and Closing Disclosure forms. |

| Break-even math | Divide the credit amount by the monthly payment increase to find how long before the higher rate costs more than you saved. |

| 2026 relevance | The term YSP is legacy, but lender credits work identically. Shopping multiple lenders remains the best defense against overpaying. |

The uncomfortable truth about "no-cost" loans

Most borrowers hear "no-cost loan" and feel relief. I understand why. Closing costs are painful, and anything that removes that pain sounds like a win. But a no-cost loan is not free. It is a loan where the cost moved from your closing table to your monthly payment for the next 30 years.

What I have seen repeatedly is that borrowers accept the no-cost framing without ever running the break-even numbers. They save $6,000 at closing and spend an extra $18,000 in interest over seven years. That is not a win. That is a trade they made without knowing the terms.

The YSP mechanism itself is not the problem. Fully disclosed YSPs are not predatory but a flexible lender tool enabling different borrower financing strategies. The problem is when borrowers do not ask the right questions. What is the par rate? What does this cost me over five years? Over ten?

My honest advice: always run the break-even calculation yourself, even if your broker does it for you. It takes ten minutes and a basic spreadsheet. And if a broker cannot or will not tell you the par rate, that is your signal to walk away. Transparency is not a courtesy in mortgage lending. It is a legal requirement. Hold your broker to it.

— LoFi

Find a transparent broker who shows you the full picture

Understanding yield spread premiums and lender credits is the first step. The second step is working with a broker who discloses everything without being asked twice.

Lofirate connects homebuyers and homeowners with licensed wholesale mortgage brokers who shop multiple lenders to find competitive pricing. Unlike retail banks that show you only their own rates, wholesale brokers give you access to a wider range of loan options and pricing structures. You can see the par rate, the lender credits, and the full cost breakdown before you commit to anything. Request a no-obligation consultation through Lofirate's broker matching service and get a second opinion on any offer you have already received. Knowing what your loan actually costs is not complicated. You just need the right broker showing you the right numbers.

FAQ

What is a yield spread premium in simple terms?

A yield spread premium is the payment a lender makes to a mortgage broker for placing your loan at an interest rate above the lender's par rate. That payment can reduce your closing costs but increases your monthly payment over the life of the loan.

Is a yield spread premium legal?

Yes. Yield spread premiums are legal when fully disclosed. The Dodd-Frank Act requires all lender-paid broker compensation to appear on your Loan Estimate and Closing Disclosure forms.

How does YSP differ from mortgage points?

Mortgage points are fees you pay upfront to lower your interest rate. A yield spread premium works in the opposite direction. You accept a higher rate and receive a credit that reduces your upfront costs.

How do i know if my loan includes a yield spread premium?

Check your Loan Estimate under the "Origination Charges" and "Lender Credits" sections. Any lender-paid broker compensation must appear there by law. If you see a lender credit listed, ask your broker to explain the rate trade-off behind it.

Should i choose a loan with or without a YSP credit?

The right choice depends on how long you plan to stay in the home. If you expect to sell or refinance within three to five years, a lender credit often makes financial sense. If you plan to stay long term, a lower rate with upfront fees typically costs less overall. Always ask your broker to show you the break-even calculation for both options.