TL;DR:

- Adjustable rate mortgages are increasingly popular in 2026, especially when fixed rates are high and short-term ownership is planned. They offer lower initial payments, but require stress-testing for potential rate increases and understanding of caps to avoid unexpected costs. Working with a licensed broker ensures accurate modeling of worst-case scenarios, helping buyers make well-informed decisions.

Adjustable rate mortgages have a reputation problem. Most people hear "adjustable" and picture risky loans that blew up during the 2008 housing crisis, leaving homeowners stuck with payments they could no longer afford. That image is outdated and, frankly, misleading for the vast majority of buyers exploring their options today. The reality is that ARMs are structured tools with built-in protections, and for the right buyer in the right situation, they can deliver meaningful savings. This guide breaks down exactly how ARMs work, why their popularity is climbing, and how to decide whether one fits your financial plan.

Table of Contents

- What is an adjustable rate mortgage?

- Why adjustable rate mortgages are gaining popularity in 2026

- ARM vs. fixed rate: Comparing mortgage options

- When should you consider an adjustable rate mortgage?

- What most guides miss about adjustable rate mortgages

- Find your best mortgage option with expert help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| ARM mechanics explained | ARMs start with a fixed rate and reset according to market indexes plus a margin. |

| Popularity rises with rates | More buyers consider ARMs when fixed-rate mortgages become expensive. |

| Risk vs reward | Lower initial payments can lead to savings, but make sure you can handle post-reset costs. |

| Comparison is key | ARMs and fixed rates serve different needs; use tables to clarify your best fit. |

| Broker guidance matters | Professional advice and rate shopping can help you maximize savings and avoid pitfalls. |

What is an adjustable rate mortgage?

An adjustable rate mortgage, or ARM, is a home loan with an interest rate that changes over time. Unlike a fixed rate mortgage where your rate stays the same for the entire loan term, an ARM starts with a fixed introductory rate for a set period, then shifts to a rate that adjusts periodically based on market conditions.

You will typically see ARMs labeled as 5/1, 7/1, or 10/1. The first number is how many years your rate stays fixed. The second number is how often the rate adjusts after that. So a 5/1 ARM gives you five years of a locked rate, then adjusts once per year after that.

Here are the key terms you need to understand before signing anything:

- Index: The benchmark rate your lender uses to calculate your new rate after the fixed period. The most common today is SOFR (Secured Overnight Financing Rate), which replaced LIBOR.

- Margin: A fixed percentage your lender adds on top of the index. If the SOFR is 4% and your margin is 2.5%, your adjusted rate would be 6.5%.

- Adjustment cap: Limits how much your rate can increase or decrease at each adjustment. A 2% cap means your rate cannot jump more than 2 points at any single adjustment.

- Lifetime cap: The maximum your rate can ever rise above the initial rate. A 5% lifetime cap means if you started at 6%, your rate can never exceed 11%.

After the initial fixed period, the ARM's rate adjusts using a published benchmark index plus a lender margin, which can raise or lower the payment depending on market rates. That two-directional movement is something many buyers overlook. Rates can actually go down post-reset too, especially if you bought when market rates were elevated.

You can explore a full mortgage terminology guide to get comfortable with all of this language before talking to a lender.

"Understanding your adjustment caps is the single most important step in evaluating any ARM. A loan with weak caps can expose you to dramatic payment swings, while one with tight caps behaves more predictably than people expect."

Pro Tip: Before you agree to any ARM, ask your lender or broker to show you the worst-case payment scenario using the lifetime cap. That number tells you the most you could ever pay each month, which is the number that really matters for your budget.

Learning about mortgage rate protection strategies early in your process helps you negotiate smarter and avoid surprises down the road.

Why adjustable rate mortgages are gaining popularity in 2026

Here is something that surprises most first-time buyers: ARMs become more attractive when fixed rates are high. That sounds backwards until you think about it. When 30-year fixed rates are elevated, the gap between a fixed rate and the lower introductory rate on an ARM widens. That gap represents real monthly savings, sometimes hundreds of dollars.

ARM market share rose from roughly 5.5% to just under 9% of new mortgages during the period tracked through late 2025, according to ABA Banking Journal. That shift reflects buyers responding rationally to higher fixed rates by choosing a product that offers immediate payment relief.

Here is what is driving the trend in 2026:

- Fixed rate mortgage payments have climbed significantly from the historic lows of 2020 and 2021, stretching affordability for many buyers

- Buyers with short-term ownership plans, typically 5 to 7 years, see ARMs as a way to capture lower payments without ever hitting the adjustment period

- Some buyers expect rates to fall over the next few years and want to benefit from that without paying refinancing costs

- Move-up buyers balancing the sale of a current home with the purchase of a new one sometimes prefer the flexibility an ARM offers during a transitional period

Understanding 2026 mortgage rate trends helps you see why the ARM calculation makes more sense now than it did when 30-year fixed rates were sitting at 3%.

"ARMs are noticeable but niche. Their share rises when payment pressure increases and drops when fixed rates become more competitive. Buyers choose them strategically, not out of desperation."

The economic logic is straightforward. A buyer locking in a 5/1 ARM at a rate meaningfully below a 30-year fixed can save thousands over five years. If they sell or refinance before year five ends, they never experience a single rate adjustment. That is not gambling. That is strategy.

Buyers exploring market trends and mortgage rates can better time and structure their loan decisions. For move-up buyers managing multiple financial goals at once, reviewing saving strategies for move-up buyers can sharpen the overall approach.

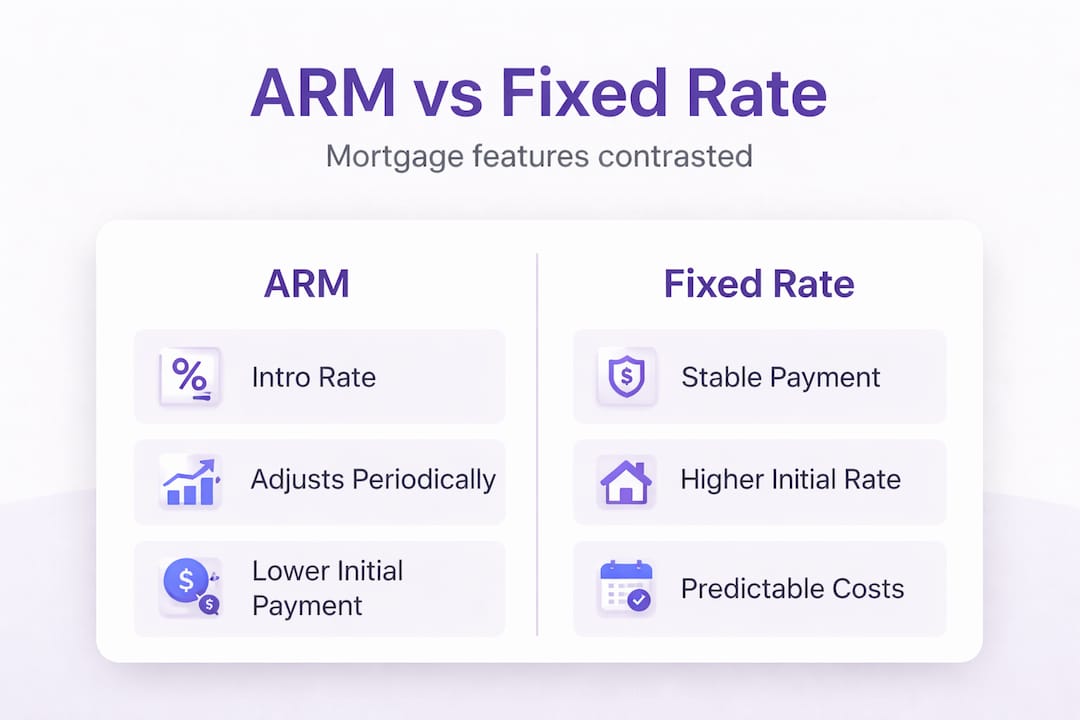

ARM vs. fixed rate: Comparing mortgage options

Choosing between an ARM and a fixed rate mortgage is not about which product is objectively better. It is about which one fits your situation. Here is a direct comparison to help you evaluate both:

| Feature | ARM | 30-year fixed |

|---|---|---|

| Initial interest rate | Lower than fixed | Higher than ARM intro rate |

| Payment predictability | Variable after fixed period | Consistent for full loan term |

| Best for short-term ownership | Yes, strong advantage | No clear advantage |

| Risk exposure | Rate increases after reset | No rate risk |

| Qualification ease | Easier with lower initial payment | Harder if rates are elevated |

| Long-term cost certainty | Lower certainty | Full certainty |

| Flexibility | More flexible if rates drop | No benefit from rate drops without refinancing |

The table makes one thing clear: neither product wins across the board. ARM share rises when payment pressure increases, which signals that buyers are making calculated trade-offs rather than avoiding risk entirely.

Here are the scenarios where each option makes sense:

- Choose a fixed rate if you plan to stay in the home for more than 10 years and value payment certainty above everything else.

- Choose a fixed rate if interest rates are historically low and locking in that rate is a clear financial win.

- Choose an ARM if you plan to sell or refinance within five to seven years and the introductory rate is meaningfully lower.

- Choose an ARM if you expect your income to grow significantly, giving you more capacity to absorb a potential rate increase.

- Choose an ARM if you want to maximize buying power today and have a clear exit strategy before the adjustment period.

After the initial fixed period, rate adjustments using a benchmark index plus lender margin can move payments in either direction. That potential for downward movement is a feature that rarely gets discussed in fixed versus ARM comparisons.

Pro Tip: If you are comparing an ARM to a fixed rate mortgage, calculate the total interest paid under both options using your expected ownership timeline, not the full loan term. Most buyers overestimate how long they will stay in a home.

A solid fixed rate mortgage guide gives you a full picture of how fixed products are structured so you can compare them accurately. Revisiting mortgage terms explained also helps you read both loan disclosures with confidence.

When should you consider an adjustable rate mortgage?

Timing and personal circumstances matter more than market conditions alone when evaluating an ARM. The product fits certain buyer profiles extremely well and fits others poorly.

Strong candidates for an ARM include:

- Buyers who plan to move within five to seven years due to career relocation, family changes, or upgrading to a larger home

- Buyers who are refinancing and expect rates to trend downward over their holding period

- High-income buyers who can absorb payment increases comfortably and want to optimize early payments

- Buyers in transitional life stages, such as newlyweds or recent graduates, who do not expect their first home to be permanent

Scenarios where you should be cautious:

- If the only way you qualify is because of the lower introductory payment, that is a warning sign worth taking seriously

- If the fully adjusted rate at the lifetime cap would make monthly payments genuinely unaffordable, the ARM is not the right fit

- If your income is unstable or you have limited emergency savings to absorb payment increases

Qualifying more easily with the lower intro payment but being unable to afford the post-reset payment creates real affordability stress, even with caps in place. CNBC is direct on this point: if the lifetime maximum would strain your budget, the ARM is not right for you.

"An ARM is a planning tool, not a shortcut. If your financial plan only works at the introductory rate, you do not have a plan. You have a gamble."

Reviewing mortgage qualification steps helps you understand where you stand before you start comparing loan products. You will also find answers to specific concerns in this list of common mortgage questions that addresses real buyer situations.

Pro Tip: Run three payment scenarios before committing to an ARM. Calculate your payment at the introductory rate, at the first adjusted rate using current index values, and at the fully capped lifetime maximum. If you can comfortably afford all three, the ARM likely works for your situation.

What most guides miss about adjustable rate mortgages

Here is what we see consistently: buyers focus on the introductory rate and stop there. They see a rate one to two percentage points below a fixed option, run the monthly payment math, and feel satisfied. What they miss is the full picture of what an ARM can do over time, good and bad.

The qualifying-at-a-lower-rate issue is more nuanced than most guides admit. Yes, a lower payment makes it easier to qualify. But lenders are required to qualify borrowers at the fully indexed rate, meaning the rate after adjustment, not just the initial rate. So if you are barely qualifying at the introductory rate, there is already a problem being flagged inside the underwriting process. The real issue is buyers who qualify technically but have not stress-tested their own budget against the worst case.

Lifetime caps also have a subtlety worth understanding. A typical cap structure is 2/2/5, meaning the first adjustment can move the rate by up to 2%, each subsequent adjustment can move it by up to 2%, and the lifetime maximum change is 5% above the starting rate. On a $400,000 loan, a 5% rate increase translates to hundreds of additional dollars per month. That is not a catastrophic scenario, but it is one you need to have a plan for.

The adjustment schedule also matters in ways that are easy to overlook. Not all ARMs adjust annually after the fixed period. Some adjust every six months. Some have specific look-back windows that determine which index value they use, which can create surprises if you are not paying attention to when adjustments happen relative to rate movements.

Our consistent advice to buyers exploring ARMs is this: ask your broker to model a worst-case payment scenario before you sign. What does your payment look like if rates rise by 5% over the adjustment lifetime? Can you absorb that, or would it require refinancing? If refinancing is the backup plan, what does the cost of that refinancing look like in that rate environment?

Understanding the full cost picture, including the smart ways to use savings and flexibility through move-up home savings, gives you a far more honest view of whether the ARM works for your long-term financial health.

Find your best mortgage option with expert help

Sorting through ARM structures, fixed rate options, and rate scenarios on your own is genuinely complicated. That is where working with a licensed wholesale mortgage broker changes the outcome.

At LoFiRate.com, we connect you with licensed wholesale brokers who shop multiple lenders to find competitive rate options, not just what one retail bank is offering today. Whether you are comparing an ARM against a 30-year fixed or exploring mortgage loan options that fit your ownership timeline, a broker can model the real numbers for your situation. The consultation is no-obligation, and getting a second opinion on your rate costs you nothing. Visit LoFiRate.com to get started, or explore our mortgage broker matching to find a licensed broker in your state who can walk you through every scenario before you commit.

Frequently asked questions

How often does the rate on an ARM change?

Most adjustable rate mortgages reset their interest rate annually after the initial fixed period, but the rate adjusts on a schedule set by your specific loan terms, so always verify your adjustment frequency with your lender.

What happens if interest rates rise significantly after my ARM resets?

Your payment could increase, but most ARMs have payment caps and lifetime maximums that limit how much the rate can climb at each adjustment and over the life of the loan.

Is it easier to qualify for an ARM than a fixed rate mortgage?

You may qualify more easily because of the lower introductory payment, but qualifying with lower intro payments can create affordability stress post-reset if your budget cannot handle the adjusted rate.

Are ARMs good for buyers planning to move soon?

ARMs can be a smart, cost-effective choice for buyers who expect to sell or refinance before the adjustment period, since buyers considering ARMs for short-term plans avoid the rate reset risk entirely by exiting the loan before it triggers.