TL;DR:

- Wholesale mortgage rates are lower because they exclude overhead costs and retail markup, saving borrowers money. Comparing rates from multiple lenders on the same day and analyzing APR ensures accurate cost assessment. Using wholesale brokers broadens loan options and offers significant long-term savings over retail rates.

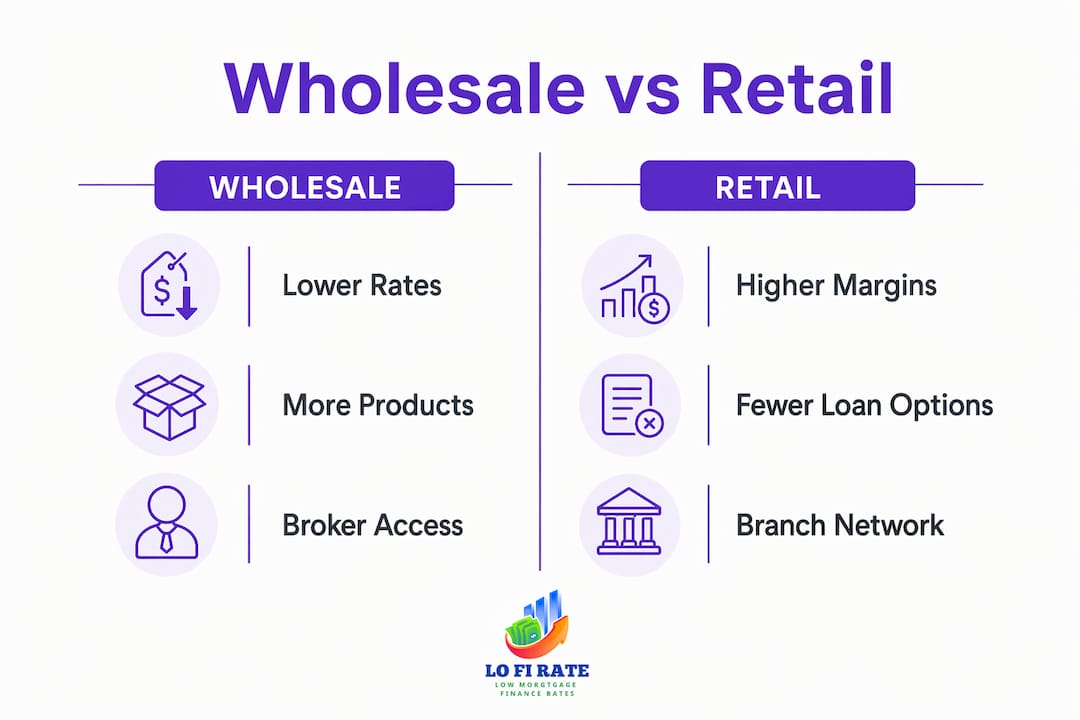

Wholesale mortgage rates are defined as the lender's base cost of funds plus a minimal margin, making them structurally cheaper than retail rates before any markup is applied. That distinction matters because retail lenders add overhead costs for branches, corporate staff, and profit targets directly into the rate you see. Wholesale rates skip most of that markup. A 0.125% to 0.50% rate difference may sound small, but on a $400,000 loan it can mean roughly $70 less per month and close to $10,000 saved over the life of the loan. Understanding why wholesale rates matter is the first step toward paying less for the same house.

Why wholesale rates matter: how they are priced differently

Wholesale mortgage rates start at the lender's cost of funds, which is tied directly to bond markets and Federal Reserve policy decisions. Lenders borrow money at a base rate, then add a margin to cover risk and profit. Retail margins vary from 0.50% in competitive markets up to 2.00% or more when lender capacity is limited. That range tells you how much room exists between what a lender pays for money and what you pay at the closing table.

Wholesale brokers operate with lower overhead than retail banks. They do not run branch networks or large corporate sales teams. That cost difference flows through to the rate. Brokers access wholesale pricing directly from lenders and pass a larger share of the margin savings to borrowers, typically 25–50 basis points below what a retail loan officer can offer.

The 30-year fixed mortgage rate typically exceeds the 10-year Treasury yield by about 1.5% to 2.5%, reflecting the added risk lenders price into long-term loans. When Treasury yields rise, mortgage rates follow. That baseline movement affects both retail and wholesale rates, but wholesale pricing stays closer to the floor because it carries less overhead markup.

Pro Tip: Ask any lender to show you their rate sheet and the margin they are adding. A wholesale broker will show you both. A retail lender typically shows you only the final rate.

Key cost drivers that separate wholesale from retail pricing:

- Bond market baseline: Both rate types start here, but wholesale stays closer to it.

- Lender margin: Retail adds 0.50%–2.00% for overhead and profit. Wholesale adds far less.

- Broker compensation: Regulated by the CFPB, so brokers cannot inflate rates to earn more.

- Operational costs: No branches means lower fixed costs passed on as savings.

What benefits do wholesale rates offer homebuyers?

The most direct benefit is a lower monthly payment from day one. A 0.50% rate difference on a $400,000 mortgage saves approximately $70 per month. Over 30 years, that compounds into roughly $10,000 in total interest savings, and that figure grows with larger loan amounts.

Beyond the rate itself, wholesale access means more loan products. Wholesale mortgage brokers can access loan products from 50 to 300+ lenders, compared to a retail bank that offers only its own internal products. That breadth matters most when your financial profile does not fit a standard mold. Self-employed borrowers, buyers with complex debt-to-income ratios, and those with non-traditional income sources often find that retail lenders decline them or impose restrictive overlays. A wholesale broker can shop across dozens of lenders to find one whose guidelines fit your situation.

The CFPB regulates broker compensation so that brokers cannot earn higher pay by steering you toward a higher-rate loan. That rule protects you. Transparency is built into the wholesale channel in a way it often is not at retail banks, where the rate markup is invisible inside the final number you receive.

Pro Tip: If you are self-employed or have a complex income history, ask a wholesale broker specifically which lenders on their panel have the most flexible underwriting guidelines. That question alone can open doors retail banks will not.

Concrete advantages wholesale access delivers:

- Lower base rate: Structurally cheaper because overhead is removed from the pricing.

- Lender variety: Access to 50–300+ lenders versus one retail bank's product menu.

- Overlay avoidance: Brokers can route around lenders with restrictive credit overlays.

- Regulated fairness: CFPB rules prevent brokers from profiting by raising your rate.

- Non-standard borrower fit: Better options for self-employed and complex-profile buyers.

You can read more about the real savings from wholesale mortgages and how brokers structure those deals for borrowers.

Why shopping multiple lenders on the same day is critical

Mortgage rates move every business day. A rate quoted on monday morning may not exist by friday afternoon. Comparing rates and APR from at least three lenders on the same day is the recommended practice for accurate rate shopping. Doing it across multiple days introduces market movement as a variable, which makes comparison meaningless.

Quote variance between lenders on identical loan profiles can exceed 0.25%. That gap represents real money over the life of a loan. The reason variance exists is that each lender prices risk differently, has different capacity constraints, and targets different borrower segments. Wholesale brokers exploit that variance by shopping your profile across their full lender panel simultaneously.

Understanding the difference between interest rate and APR is also critical when comparing quotes. The interest rate tells you the cost of borrowing. The APR includes fees, points, and other costs rolled into an annualized figure. Two loans with the same interest rate can carry very different APRs. You can get a clear breakdown of APR versus interest rate before you start comparing quotes.

Here is the right sequence for rate shopping:

- Pull your credit once. Multiple mortgage inquiries within a 14-to-45-day window count as a single inquiry under FICO scoring rules.

- Request quotes from at least three sources on the same day. Include at least one wholesale broker in that group.

- Compare APR, not just rate. A lower rate with high fees can cost more than a slightly higher rate with no points.

- Lock quickly when you find a favorable rate. Waiting for a lower rate can result in higher home prices and fewer inventory options.

- Use a checklist. A structured mortgage shopping checklist keeps your comparisons consistent across lenders.

Pro Tip: Get all quotes on the same loan structure: same loan amount, same down payment, same loan term. Changing any variable makes the comparison unreliable.

How wholesale rates affect long-term affordability and wealth

The monthly savings from a lower rate are visible immediately. The wealth-building effect takes longer to see but is far larger. A borrower who saves $70 per month on a $400,000 loan has $840 more per year. Over 30 years, that is $25,200 in cash that stayed in their pocket rather than going to the lender, before accounting for what that money could earn if invested.

The compounding effect of a lower rate also reduces the total interest paid over the loan's life. On a 30-year fixed mortgage, the majority of early payments go toward interest rather than principal. A lower starting rate means less interest accrues in those early years, which accelerates equity building.

| Loan Amount | Rate Difference | Monthly Savings | Estimated Lifetime Savings |

|---|---|---|---|

| $300,000 | 0.25% | ~$40 | ~$7,500 |

| $400,000 | 0.50% | ~$70 | ~$10,000+ |

| $500,000 | 0.50% | ~$90 | ~$13,000+ |

Estimates are illustrative and vary based on rate environment and loan term.

Borrowers who shop mortgage rates aggressively and lock quickly when favorable rates appear save tens of thousands over a 30-year loan. That is not a theoretical outcome. It is the direct result of starting with a lower base rate and maintaining it for the full loan term.

The savings also create options. A borrower paying $70 less per month can redirect that amount toward extra principal payments, which shortens the loan term and reduces total interest further. Alternatively, that money can go into a retirement account or emergency fund. The rate you lock today shapes your financial flexibility for decades. Understanding the full impact of retail versus wholesale pricing makes the choice clearer.

Key Takeaways

Wholesale mortgage rates deliver structurally lower costs than retail rates because they remove branch overhead and corporate markup from the pricing, giving borrowers a direct path to the lender's base cost of funds.

| Point | Details |

|---|---|

| Wholesale rates start lower | Retail adds 0.50%–2.00% in margin; wholesale skips most of that markup. |

| Savings are real and large | A 0.50% rate difference on $400,000 saves roughly $10,000 over the loan's life. |

| Broker access is broader | Wholesale brokers shop 50–300+ lenders; retail banks offer only their own products. |

| Same-day shopping is required | Rate quotes shift daily; comparing three or more lenders on the same day gives accurate pricing. |

| APR reveals the true cost | Always compare APR alongside the interest rate to account for fees and points. |

What I have learned from watching borrowers overpay

Most homebuyers walk into a retail bank because it feels familiar. They have a checking account there, they trust the brand, and the loan officer seems helpful. What they do not see is the markup baked into the rate before the conversation even starts.

I have seen borrowers accept a rate 0.375% above what a wholesale broker could have offered on the same day, for the same loan, with the same credit profile. That gap does not feel significant in the moment. Over 30 years, it is a car payment that never ends.

The uncomfortable truth about retail mortgage pricing is that the bank's goal is not to find you the lowest rate. Its goal is to close the loan at the highest rate you will accept. Wholesale brokers operate differently because their business model depends on repeat referrals and competitive pricing, not on a single transaction margin.

Proactive borrowers who understand rate shopping and use a wholesale broker consistently come out ahead. The ones who do not are often surprised years later when they refinance and realize what they were paying. The information to make a better choice is available. The only question is whether you use it before you sign.

— LoFi

Access wholesale mortgage rates through Lofirate

Lofirate connects homebuyers and homeowners directly with licensed wholesale mortgage brokers in their state. Retail lenders show you one rate. Lofirate's broker network shops dozens of lenders to find pricing that reflects the wholesale market, not a single bank's markup.

The process is straightforward. You request a consultation, a licensed broker reviews your profile, and you receive competitive rate options with no obligation. Whether you are buying your first home or refinancing an existing loan, wholesale broker matching through Lofirate gives you access to pricing most retail borrowers never see. You can also review available loan options to find the right fit for your financial profile. Visit Lofirate to get started.

FAQ

What are wholesale mortgage rates?

Wholesale mortgage rates are the rates lenders offer directly to mortgage brokers, before retail markup is added. They reflect the lender's base cost of funds plus a smaller margin than retail pricing.

How much can I save with a wholesale mortgage rate?

A rate difference of 0.50% on a $400,000 mortgage saves approximately $70 per month and roughly $10,000 over the life of the loan, depending on the rate environment and loan term.

Why should I use a wholesale mortgage broker?

Wholesale brokers access loan products from 50 to 300+ lenders and are regulated by the CFPB to prevent rate steering. That combination gives you broader options and built-in consumer protection.

How do I compare mortgage rates accurately?

Request quotes from at least three lenders on the same day and compare APR, not just the interest rate. APR includes fees and points, which makes it a more complete measure of total loan cost.

Does shopping multiple lenders hurt my credit score?

Multiple mortgage inquiries within a 14-to-45-day window are treated as a single inquiry under FICO scoring rules. Shopping aggressively within that window does not damage your credit.