TL;DR:

- Retail mortgage rates include high overhead costs, making them significantly more expensive.

- Wholesale brokers offer lower rates by competing lenders, saving borrowers thousands over the loan life.

- Comparing retail and wholesale options is essential to avoid overpaying and find the best mortgage deal.

Most homebuyers walk into their bank, accept the rate they're offered, and move on. It feels safe. It feels familiar. But that comfort could be costing you tens of thousands of dollars over the life of your loan. Retail mortgage rates carry hidden overhead that you pay for whether you realize it or not. Wholesale brokers offer a different path, one where multiple lenders compete for your business instead of you accepting whatever one institution decides to charge. This guide breaks down exactly why retail rates run higher, how wholesale brokers work, and what the real savings look like in dollars.

Table of Contents

- What are retail mortgage rates and why are they higher?

- How wholesale brokers get you better rates and more choices

- Real-world savings: How much can you save by avoiding retail rates?

- Is wholesale always better? When retail rates do make sense

- Why most homebuyers overpay (and how to break the cycle)

- Find your best rate with a wholesale broker today

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Retail rates are higher | Banks add costs from overhead and pass them along to you in the form of higher rates. |

| Wholesale brokers create competition | Brokers shop many lenders at once, driving down your potential rate by letting banks compete for your loan. |

| You can save thousands | Using a wholesale broker can save you $10,000 to $44,000 over the life of your mortgage. |

| Compare both options | For the best deal, always compare wholesale broker offers to your bank's retail rate before committing. |

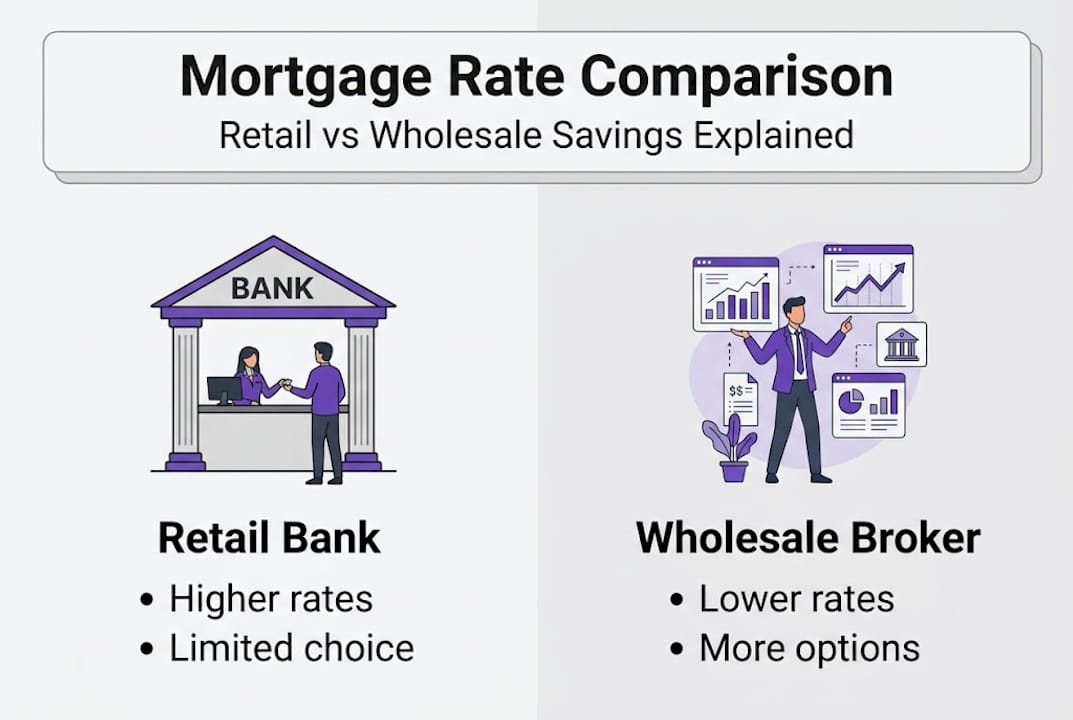

What are retail mortgage rates and why are they higher?

A retail mortgage rate is the interest rate a bank or direct lender quotes you when you walk in as a customer. The bank originates the loan, services it, and profits from the spread between what it costs them to borrow money and what they charge you. Simple enough. But the rate you see is not just a reflection of market conditions. It also reflects every cost the bank carries to operate.

Think about what a major bank maintains: thousands of branch locations, armies of loan officers, national television advertising, ATM networks, and layers of corporate management. All of that overhead gets baked into your mortgage rate. Retail mortgage rates are higher due to embedded overhead costs like branch networks, national advertising, ATM infrastructure, and corporate structures, which are passed on to consumers.

Here is where the numbers get eye-opening. Retail banks carry margins of 4.5% to 6%, while wholesale lending is capped at 2.75% by federal regulation. That gap is not a coincidence. It is a structural feature of how retail lending works.

The major cost drivers that inflate retail mortgage rates include:

- Branch network maintenance across hundreds or thousands of locations

- National and local advertising campaigns that run year-round

- Corporate overhead including executive compensation and administrative layers

- ATM and banking infrastructure unrelated to mortgage lending

- Loan officer salaries paid regardless of loan volume

Wholesale brokers sidestep most of these costs. They operate lean businesses focused entirely on connecting borrowers with lenders, which is why they can access pricing that retail banks simply cannot match for most borrowers. Understanding mortgage rate transparency is the first step toward knowing whether you are getting a fair deal.

As one industry analyst put it:

"The retail mortgage model was built for a different era. Today's borrowers have access to wholesale pricing that strips out the institutional overhead, and most of them don't even know it exists."

If you want to understand where 2026 mortgage trends are heading, the continued growth of wholesale lending is one of the most important shifts to watch. According to Bankrate on wholesale lenders, the wholesale channel has been expanding steadily as more borrowers discover the pricing advantage.

How wholesale brokers get you better rates and more choices

A wholesale mortgage broker does not lend you money directly. Instead, the broker acts as your advocate, submitting your loan to dozens of wholesale lenders who compete to win your business. That competition is what drives rates down.

Where a retail bank can only offer its own products at its own pricing, a broker can shop mortgage lenders across a wide network. Wholesale brokers access 50 or more lenders, enabling competition that drives lower rates, typically 0.125% to 0.50% lower, and more loan options including non-QM, jumbo, and bank statement loans for self-employed borrowers.

| Feature | Retail bank | Wholesale broker |

|---|---|---|

| Lenders available | 1 | 50 or more |

| Rate competition | None | Active bidding |

| Loan product variety | Limited | Broad |

| Overhead passed to borrower | Yes | Minimal |

| Best for | Simple, standard loans | Complex or cost-sensitive needs |

The process of getting a brokered mortgage works like this:

- You apply with a licensed broker and share your financial profile

- The broker submits your file to multiple wholesale lenders simultaneously

- Lenders compete and return rate quotes

- The broker presents your best options with full fee disclosure

- You choose the loan that fits your goals

- The broker manages the process through to closing

This structure creates real leverage for you as a borrower. The brokered loan benefits extend beyond rate savings too. Brokers often have access to specialized programs that retail banks do not offer, including products for borrowers with recent credit events, investors, or those with non-traditional income.

Pro Tip: Ask your broker specifically about niche programs for your situation. If you are self-employed, a veteran, or buying a non-warrantable condo, there may be a wholesale product designed exactly for your needs that no retail bank will show you.

For first-time buyers especially, the wholesale advantages are significant. You are entering the market without an established banking relationship that might earn you a loyalty discount, which means you have everything to gain from letting lenders compete.

Real-world savings: How much can you save by avoiding retail rates?

Understanding the broker advantage is one thing. Seeing the numbers drives home the point. Here is what you could actually save.

Borrowers save significantly with wholesale access: roughly $10,000 as a lifetime average, up to $44,000 by shopping lenders, and one concrete example shows $23,260 in savings over 30 years on a $400,000 loan after fees. According to Realtor.com lending savings data, shopping around for a lender could save borrowers up to $44,000 over the life of a 30-year loan.

| Loan amount | Rate difference | Monthly savings | 30-year savings |

|---|---|---|---|

| $250,000 | 0.25% | ~$37 | ~$13,300 |

| $400,000 | 0.25% | ~$59 | ~$21,200 |

| $600,000 | 0.375% | ~$133 | ~$47,900 |

| $800,000 | 0.50% | ~$237 | ~$85,300 |

The hidden costs you avoid by going wholesale go beyond the interest rate itself:

- Rate lock fees that some retail banks charge upfront

- Application and processing fees bundled into retail pricing

- Higher discount points required to buy down a retail rate

- Origination fees that reflect institutional overhead

- Inflated third-party service costs steered by the lender

The wholesale channel now represents 26% of all mortgage originations in 2025, up from 19% in 2020 according to HMDA data, with rates running 0.125% to 0.50% lower than retail. That growth is not accidental. Borrowers who discover wholesale pricing tend not to go back.

For first-time buyers, the math is especially compelling. You are likely taking on the largest debt of your life. Even a 0.25% rate improvement on a $400,000 loan saves you more than $21,000 over 30 years. Strategies for finding competitive mortgage rate tips and understanding lender competition can make that difference real for you.

Is wholesale always better? When retail rates do make sense

Wholesale is powerful but not perfect. Let's cover when retail banking might actually be your best move.

Retail lenders do have genuine advantages in certain situations. Retail works better for simple cases with existing bank relationships, offering faster processing, more direct control, and no broker fees. If you have an 800 credit score, a standard W-2 income, and a straightforward conforming loan, your bank might match or beat what a broker finds.

Borrowers who may do just as well with retail include:

- Existing bank clients with loyalty rate discounts or relationship pricing

- Borrowers with exceptional credit who qualify for a bank's best advertised rates

- Buyers needing very fast closings where the bank's internal process is faster

- Those with simple, conforming loan needs where competition matters less

- Borrowers who prefer direct lender relationships for servicing continuity

On the other side, wholesale clearly wins for complex scenarios. Self-employed borrowers, jumbo loan buyers, those with recent credit challenges, and investors with non-standard properties will almost always find better options through a broker.

The cons of wholesale are real and worth knowing: broker fees ranging from 0.5% to 2%, the likelihood that your loan will be sold and your servicer will change after closing, and less direct control over the origination process.

Knowing what brokers do helps you set the right expectations before you start. And reviewing the questions for your broker before your first meeting ensures you get the information you need to compare fairly.

Pro Tip: Always get a loan estimate from both a retail lender and a wholesale broker before making your decision. The comparison takes a few days and could save you thousands. The bank or broker comparison is worth doing every single time.

Why most homebuyers overpay (and how to break the cycle)

Here is the uncomfortable truth: most homebuyers do not overpay because they are careless. They overpay because the system is designed to make retail feel like the obvious choice.

Your bank is familiar. You trust it. The loan officer is friendly and the process feels simple. That comfort is worth something, but it should not cost you $20,000 or more over the life of your loan.

Analysis paralysis plays a role too. When buyers feel overwhelmed by the mortgage process, they default to the path of least resistance. One quote feels like enough. But mortgage competition strategies show that comparison shopping is the single strongest predictor of mortgage savings, stronger than credit score improvements or down payment size in many cases.

The counterintuitive lesson here is that one phone call to a wholesale broker is often all it takes to change your financial picture. You do not have to commit. You do not have to switch. You just have to compare. Buyers who break the habit of defaulting to their retail bank consistently come out ahead, and the ones who do not often spend years wondering why their neighbor refinanced at a lower rate.

Find your best rate with a wholesale broker today

You now know why retail rates run higher, how wholesale brokers create real competition for your loan, and what the savings can look like over time. The next step is putting that knowledge to work.

LoFiRate connects homebuyers and homeowners with licensed wholesale mortgage brokers in their state, no obligation, no pressure, just transparent access to competitive pricing. Whether you are buying your first home or refinancing an existing loan, exploring broker matching services takes minutes and could save you thousands. Check out the available loan options and request a free consultation today. The rate you were quoted at the bank may not be the best rate available to you.

Frequently asked questions

What are retail mortgage rates?

Retail mortgage rates are set by banks and lenders that deal directly with consumers and generally include higher costs due to branch and operational expenses. Retail rates are higher because embedded overhead costs are passed directly to the borrower.

How much can I save by avoiding retail mortgage rates?

Homebuyers can save an average of $10,000 over the life of their loan, and sometimes up to $44,000, by using wholesale brokers instead of accepting retail rates.

When do retail mortgage rates make sense?

Retail rates can be a good option for simple loan scenarios when you have excellent credit or a strong relationship with your bank. Retail works best when faster processing and no broker fees outweigh the potential rate savings from shopping wholesale.

What are the downsides of using a wholesale broker?

Wholesale brokers may charge fees of 0.5% to 2% and your loan servicer can change after closing, which some borrowers find disruptive.

Do mortgage brokers always beat retail rates?

Not always. Sometimes a retail bank can match or beat broker rates, so it is smart to compare both channels before making your final decision.