TL;DR:

- Second home loans have stricter qualification criteria and higher interest rates than primary mortgages.

- They require personal use certification and have specific rules on rental and occupancy.

- Working with a wholesale broker helps find better rates and tailored financing options.

Buying a second home feels exciting right up until your lender hands you a completely different set of rules than the ones you remember from your first mortgage. Many homeowners walk in expecting a familiar process and walk out confused about reserve requirements, occupancy rules, and why their rate is suddenly higher. The truth is, second home loans operate under their own set of guidelines, and understanding those differences before you apply can save you money, time, and a lot of frustration.

Table of Contents

- What is a second home loan?

- How do you qualify? Key requirements and challenges

- Second home loan vs. other options: How do they compare?

- Managing two mortgages: Risks, strategies, and refinancing

- Our perspective: What most guides miss about second home loans

- Find your best second home loan option today

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Second home loan basics | A second home loan allows you to finance a property you intend to use for personal enjoyment, not as an investment. |

| Qualification differences | Lenders expect higher down payments and stronger finances than for your first mortgage. |

| Compare all options | Weigh second home loans against refinancing and investment property loans to choose the best fit. |

| Understand the risks | Managing two mortgages means carefully planning for vacancies, higher rates, and emergencies. |

| Wholesale brokers matter | Partnering with a broker can help you access lower rates and more creative loan solutions. |

What is a second home loan?

A second home loan is a mortgage used to purchase a property that is not your primary residence but is also not classified as a rental or investment property. That middle-ground distinction matters more than most buyers realize. Lenders treat second homes differently from both your main residence and from properties you plan to rent out for income. The category you fall into directly shapes your interest rate, down payment, and qualification requirements.

The types of properties that qualify as second homes are broader than you might expect. Think of a lakeside cabin you visit in the summer, a beach condo used on weekends, an urban patio home near family, or a mountain retreat for ski season. What ties them together is personal use. You, as the owner, must occupy the property for a meaningful portion of the year. Lenders will often ask you to certify that the home will not be rented full-time or managed as an income-generating asset.

The most common reasons homeowners pursue a second home loan include:

- Building long-term wealth through real estate equity

- Creating a dedicated vacation space without paying hotel costs year after year

- Planning ahead for retirement by purchasing in a desired location early

- Staying near family in another city without committing to a permanent move

- Enjoying potential appreciation in a desirable market

A second home must typically be a single-unit property that you occupy for personal use. It cannot be subject to a timeshare arrangement or managed by a rental company on your behalf full-time. This is a bright-line rule that many lenders enforce strictly.

One of the most common misconceptions is that a vacation home and an investment property are the same thing. They are not. Exploring the full range of types of mortgage loans available will show you just how distinct these categories are in practice. The loan product you choose shapes everything from your tax deductions to your ability to list the home on short-term rental platforms.

With the basics outlined, the next step is understanding how qualification for a second home loan differs from your first mortgage.

How do you qualify? Key requirements and challenges

Qualifying for a second home loan is meaningfully harder than qualifying for a primary residence. Lenders view a second mortgage as higher risk because, if finances get tight, most borrowers prioritize their main home payment first. That logic shapes every requirement you will face.

Here is a clear breakdown of what most lenders expect for second home mortgage qualification:

- Credit score: A minimum score of 680 is common, though many lenders prefer 720 or higher to offer competitive rates. The higher your score, the better the pricing you will see.

- Debt-to-income ratio (DTI): Lenders typically cap your total monthly debt obligations at 43% to 45% of your gross monthly income, and that now includes both your primary and your second home mortgage payment.

- Down payment: Most lenders require at least 10% down, and a 20% or larger down payment often unlocks better rates and eliminates private mortgage insurance (PMI).

- Cash reserves: After closing, you may be required to show that you have between two and six months of mortgage payments sitting in liquid savings for both properties combined.

- Income documentation: Expect to provide recent pay stubs, two years of tax returns, and possibly additional documentation if you are self-employed or have variable income.

The part that surprises most applicants is the occupancy certification. Lenders will ask you to confirm, in writing, that the property is for your personal use and not a full-time rental. If a lender later discovers you are operating the home primarily as a rental, it can be treated as mortgage fraud. Understanding the full home loan application process helps you prepare the right documentation from the start and avoid any misrepresentation issues.

Pro Tip: If you plan to rent the property out occasionally on platforms like Airbnb, talk to your lender before closing. Some lenders permit limited short-term rentals as long as personal use is the primary purpose. Others do not allow it at all. Getting clarity upfront prevents costly surprises later.

Another common stumbling block is underestimating how the second payment affects your DTI. Even if your income is strong, carrying two mortgage payments can push your DTI close to the threshold, making lenders nervous. A higher down payment or paying down other debts before applying can bring that ratio back into an acceptable range.

Now that you know the hurdles to qualifying, it is important to see how second home loans stack up against other popular options.

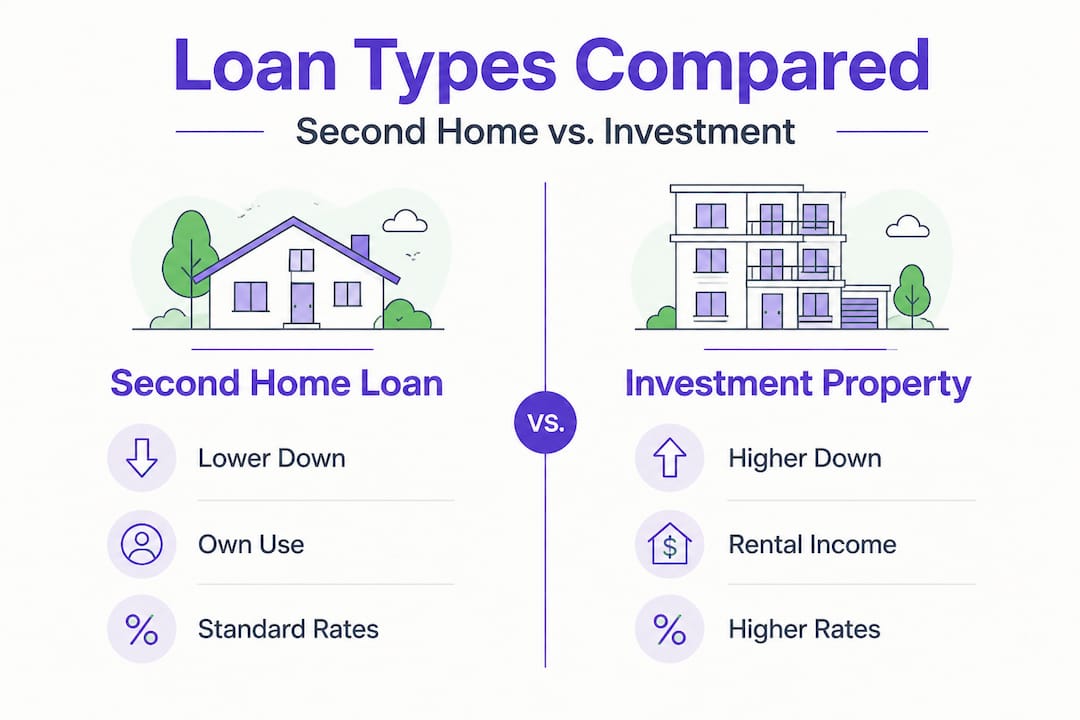

Second home loan vs. other options: How do they compare?

Understanding where a second home loan fits in the broader landscape of real estate financing helps you make a genuinely informed decision. Not everyone who wants a second property is best served by a traditional second home mortgage. Sometimes a cash-out refinance on your existing home or an investment property loan makes more sense depending on your goals.

Here is a feature-by-feature comparison of the three most common paths:

| Feature | Second home loan | Investment property loan | Cash-out refinance |

|---|---|---|---|

| Minimum down payment | 10% | 15% to 25% | Varies (based on equity) |

| Interest rate | Slightly above primary | Highest of the three | Based on primary home rate |

| Rental income allowed | No | Yes | Not applicable |

| Occupancy required | Yes, personal use | No | Primary residence |

| PMI required | Possibly | Rarely | Possibly |

| Tax deduction on interest | Yes | Yes (as expense) | Sometimes |

The differences in interest rates are worth examining closely. Investment property loans typically carry rates that are 0.50% to 0.875% higher than second home loans, because lenders see them as higher risk. A cash-out refinance on your primary home often comes with the lowest rate of all three since it is secured by the property you live in.

Tax implications also vary significantly. Second home mortgage interest is generally deductible on federal taxes, subject to the same total mortgage debt limits as your primary residence. Investment property loan interest is deductible as a business expense, which works differently. Reviewing types of homebuyer programs can help you see how various loan products intersect with tax strategy and long-term financial planning.

Key reasons to consider working with a wholesale broker for this decision:

- Brokers have access to multiple lenders and can compare pricing across options you cannot access directly

- Wholesale pricing often beats retail bank pricing on the same loan product

- A broker can help you correctly categorize the property to avoid misclassification issues

- They can model out total cost comparisons across all three financing paths for your specific numbers

Understanding how brokers help rates gives you a clear picture of why working with a wholesale broker is often the smartest move for any complex real estate financing situation.

With this context, let's look at the unique challenges of managing multiple mortgages and what you can do to stay financially healthy.

Managing two mortgages: Risks, strategies, and refinancing

Running two mortgages simultaneously is a financial commitment that carries real risks, and most buyers underestimate how quickly those risks can compound. Here is a realistic look at what you may face:

Liquidity risk: If you have most of your savings tied up in equity, a sudden repair bill or a period of unemployment can put both payments at risk simultaneously.

Vacancy: If you planned to offset some costs through occasional rentals and the property sits empty, your budget takes a hit with no revenue to compensate.

Rate changes: If either loan is on an adjustable-rate mortgage (ARM), a rate reset can increase your monthly payment in ways that strain your DTI.

Unexpected expenses: A second property in a different climate or geography may face maintenance costs you did not anticipate, from hurricane prep to snow removal to higher insurance premiums.

Here is a snapshot of how financial exposure grows with two mortgages:

| Scenario | Monthly impact | Annual risk exposure |

|---|---|---|

| Both loans at fixed rate | Predictable and stable | Lower risk if reserves are solid |

| One ARM, one fixed | Variable on one payment | Moderate, depends on rate cap |

| Both loans on ARM | Unpredictable and compounding | High risk without cash cushion |

| Rental income offsetting second | Income dependent | Medium, vacancy creates gaps |

To manage these risks effectively, consider these strategies:

- Build a dedicated emergency fund with at least six months of combined mortgage payments before closing on your second home

- Get landlord or vacant home insurance if the property will sit unoccupied for long stretches

- Review refinancing strategies annually to see if locking in a lower rate would reduce your total payment exposure

- Use a broker to monitor wholesale rate movement so you can refinance at the right moment, not just when a retail bank sends you a flyer

Pro Tip: Many owners of second homes wait too long to refinance because they assume their situation is too complex. In reality, mortgage competition benefits borrowers most when the situation is complicated. More lenders competing for your loan means more pressure on pricing, and a skilled broker is the one making that competition happen on your behalf.

Refinancing a second home also follows different rules than refinancing an investment property, which is important if you are comparing your options or thinking about reclassifying your property. Keeping those distinctions clear will protect your loan terms and your legal standing with your lender.

After exploring practical management, it is helpful to see the bigger picture and get an expert perspective on what most guides overlook.

Our perspective: What most guides miss about second home loans

Most articles on second home loans stop at the qualification checklist and the rate comparison table. We think that leaves buyers genuinely underprepared for what comes next.

The real cost of a second home loan does not fully show itself at closing. It shows up three years in, when an unexpected roof issue hits your mountain cabin the same month your adjustable rate ticks up. Or when you realize the property you bought for retirement lifestyle purposes is actually costing you flexibility in every other area of your financial life. These are not reasons to avoid a second home. They are reasons to go in with your eyes open and a clear financial plan.

Here is what we believe most buyers miss: the strategy matters more than the rate. A slightly higher rate on a well-structured loan, with the right reserves and a clear refinancing roadmap, is far better than a slightly lower rate on a loan that leaves you financially exposed. Too many buyers are so focused on the purchase itself that they do not think about the three to five year plan for that loan.

Working with a broker who understands brokered loan strategies is not just about getting a lower rate today. It is about having someone in your corner who can help you time a refinance, identify when your equity position has improved enough to change your terms, and who is not incentivized to sell you a single product from a single institution.

Retail banks offer one menu. Wholesale brokers bring the whole marketplace to your table. For a transaction as significant and long-term as a second home loan, that difference matters enormously.

Find your best second home loan option today

A second home is one of the most meaningful financial commitments you can make, and the financing behind it deserves the same care as the property itself. At LoFiRate.com, we connect homeowners like you with licensed wholesale mortgage brokers who shop multiple lenders to find the most competitive options available for your specific situation.

Whether you are purchasing your first vacation property or refinancing an existing second home, our mortgage broker services are built to give you real pricing options, not a single take-it-or-leave-it rate from a retail bank. You can also compare loan options across different product types to see which path fits your goals and budget. There is no obligation to proceed, just a clear conversation with a licensed professional who can help you understand what you actually qualify for and what your options are.

Frequently asked questions

Can you use rental income to qualify for a second home loan?

Most lenders do not count projected rental income when qualifying you for a second home loan. Only investment property loans allow rental income to offset your debt-to-income ratio during underwriting.

What is the minimum down payment for a second home loan?

Most lenders require at least 10% down for a second home loan, though some ask for 20% or more depending on your credit profile. A stronger down payment often reduces your rate and eliminates PMI, as outlined in this mortgage qualification guide.

How does refinancing work for a second home?

You can refinance your second home to lower your rate or access equity, but lenders typically apply stricter guidelines than for a primary residence. For a detailed comparison, the guide on how to refinance covers the key steps and requirements.

Will a second home loan affect my ability to get other loans?

Yes, a second home loan adds to your total monthly debt obligations, which raises your DTI and can limit approval for future credit. Review your full mortgage qualification picture before taking on any additional financing.

Are rates higher for second home loans?

Interest rates for second home loans are generally slightly higher than for primary residences but meaningfully lower than for investment property loans. Reviewing your full range of loan options with a broker helps you find the most competitive pricing available for your situation.