TL;DR:

- Mortgage contingency clauses allow buyers to exit without losing deposits if financing falls through.

- Meeting strict deadlines is essential to retain protection and avoid losing deposits.

- Negotiating flexible terms and working with experienced lenders enhances buyer safety and competitiveness.

Your offer just got accepted. Champagne moment, right? Not quite. Many buyers assume the hard part is over once a seller says yes, but the real financial risk is still sitting right there in the contract. A mortgage contingency clause is one of the most powerful protections available to homebuyers in the U.S., yet it's routinely misunderstood, rushed through, or worse, waived entirely under competitive pressure. This guide breaks down exactly how mortgage contingency works, the concrete ways it shields your deposit, the deadlines you cannot afford to miss, and how to negotiate smarter terms in any market.

Table of Contents

- Understanding mortgage contingency clauses

- How mortgage contingency protects buyers

- Important deadlines and steps in mortgage contingency

- Negotiating and optimizing mortgage contingency terms

- Our perspective: Why mortgage contingency is your real safety net

- Explore your mortgage options with LoFi Rate

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Protects buyers' deposits | Mortgage contingency gives buyers a way to recover their deposit if financing fails, reducing risk during homebuying. |

| Deadlines are critical | Meeting all contingency deadlines is essential to avoid losing your deposit and jeopardizing the purchase. |

| Negotiation strengthens outcomes | Careful negotiation of contingency terms can make your offer more appealing and better protect your interests. |

| Consult experts | Working with brokers and lenders helps optimize mortgage contingency clauses and successfully close your deal. |

Understanding mortgage contingency clauses

A mortgage contingency is a clause written into a home purchase contract that gives you the legal right to walk away from the deal without losing your earnest money deposit if you cannot secure a mortgage loan within a set timeframe. It's a conditional agreement. The sale only moves forward if your financing comes through. Think of it as a financial escape hatch built directly into the contract.

This clause appears in the purchase and sale agreement, typically under a section labeled "financing contingency" or "loan contingency." It spells out the loan amount you need, the type of loan (conventional, FHA, VA), the maximum interest rate you'll accept, and the deadline by which your lender must issue a commitment letter. If any of those conditions aren't met, the contingency can be triggered.

Here's what the clause typically covers:

- Loan amount: The minimum amount you need to borrow

- Loan type: Conventional, FHA, or VA, as specified

- Interest rate cap: The highest rate you're willing to accept

- Deadline: How many days you have to secure financing, usually 21 to 45 days

- Commitment letter: Written proof from your lender that the loan is approved

A real-world example: You agree to buy a home for $450,000. You put down $15,000 in earnest money. Your mortgage contingency states you need a $360,000 loan at no more than 7.5% within 30 days. Your lender runs into an appraisal issue and denies the loan. Without contingency, you'd lose that $15,000. With it, mortgage contingency allows buyers to back out without penalty if they can't secure financing.

Mortgage contingency is not just a formality. It's a contractual shield that keeps your deposit safe when lenders say no.

Understanding mortgage compliance protections in your state also matters because some states have specific rules around how contingencies must be written and disclosed. And if you're unsure whether your offer is priced right, reviewing mortgage rate transparency practices helps you evaluate lender terms before you ever sign.

How mortgage contingency protects buyers

The most direct protection is simple: you get your money back. If your financing falls through within the contingency period, buyers may walk away with their deposit if financing falls through, thanks to mortgage contingency. That could be thousands of dollars you'd otherwise lose forever.

But the protection runs deeper than just the deposit. It also gives you time to shop lenders without panicking. If your first lender declines, you can pivot to a different one, all while staying legally protected under the contract.

Here's a side-by-side look at the risk difference:

| Scenario | With mortgage contingency | Without mortgage contingency |

|---|---|---|

| Lender denies loan | Deposit returned, no penalty | Deposit forfeited |

| Appraisal comes in low | Can renegotiate or exit safely | Stuck in contract |

| Rate spikes above cap | Contingency triggered, buyer exits | No protection |

| Buyer finds better lender | Time to pivot within deadline | Risk of delay and loss |

Mortgage contingency is a common contract feature in U.S. real estate transactions, though its terms vary widely by state and market.

Sellers aren't entirely disadvantaged either. A buyer with a solid pre-approval and a tight contingency window can actually strengthen their offer because it signals readiness. Sellers prefer this over buyers who look financially shaky.

Here's what buyers should watch for:

- Review contingency dates the moment you receive the signed contract

- Confirm your lender's timeline matches the contract deadline

- Check whether your contingency requires a commitment letter or just an approval

- Use a mortgage shopping checklist to stay organized across lenders

Pro Tip: Before signing anything, cross-reference the contingency deadline with your lender's processing timeline. Lenders often need 30 to 45 days minimum. A 21-day contingency with a slow underwriter is a recipe for losing your deposit.

Also, know how navigating mortgage compliance requirements can affect approval timing in your state. Regulatory steps like appraisal reviews and income verification can add days you haven't accounted for.

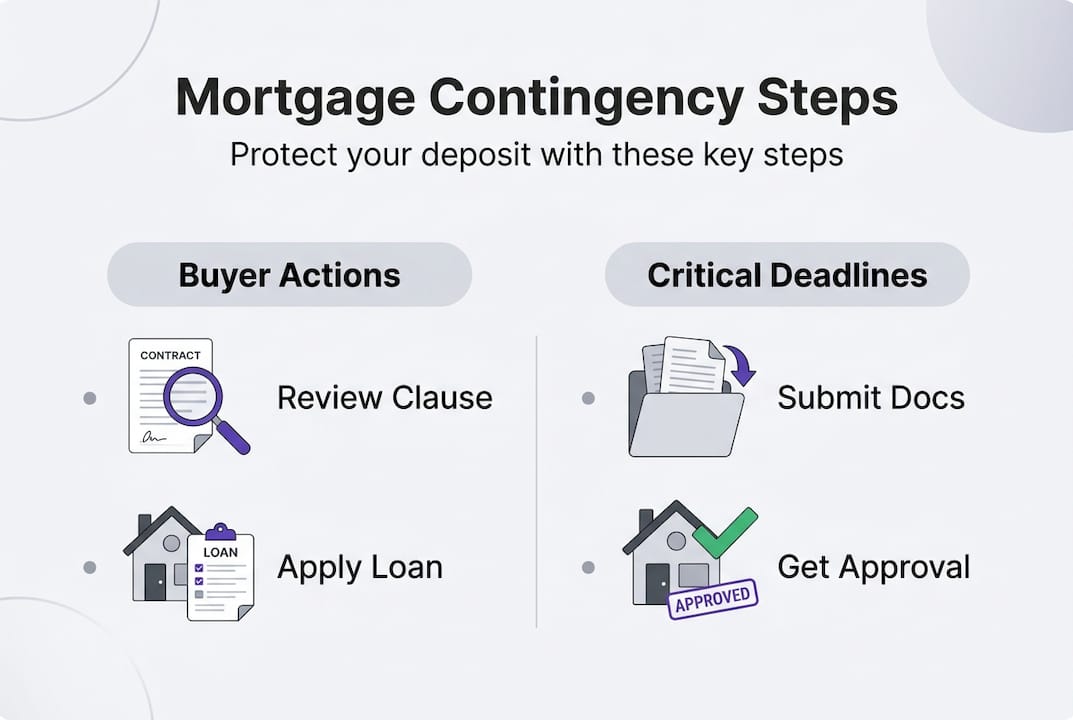

Important deadlines and steps in mortgage contingency

Knowing that mortgage contingency offers protection is only half the picture. Keeping track of the critical deadlines is where buyers often stumble.

Mortgage contingency clauses include strict deadlines that buyers must meet, and missing them can cost you the deal and your deposit. The clock starts the moment both parties sign the contract, not when you feel ready.

Here's a typical timeline for meeting your mortgage contingency:

- Day 1 to 3: Submit your full mortgage application immediately after signing the purchase contract

- Day 3 to 7: Provide all required documents, pay stubs, tax returns, bank statements, and ID

- Day 7 to 14: Lender orders an appraisal of the property

- Day 14 to 21: Underwriter reviews your file and the appraisal report

- Day 21 to 30: Lender issues commitment letter (or conditional approval with remaining items)

- Day 30 to 45: Final loan approval and preparation for closing

Here's a data table showing how contingency periods compare by market type:

| Market condition | Typical contingency period | Buyer risk level |

|---|---|---|

| Buyer's market | 30 to 45 days | Low |

| Balanced market | 21 to 30 days | Moderate |

| Seller's market | 14 to 21 days | High |

| Competitive bidding | 10 to 14 days | Very high |

If you miss the contingency deadline, you lose your contingency protection. The seller can keep your deposit and potentially cancel the deal. Some contracts allow for extensions if both parties agree in writing, but sellers in hot markets have little reason to give you extra time.

Pro Tip: Don't wait for your lender to ask for documents. Gather everything before you even make an offer. A well-prepared mortgage pre-approval process means your lender can move faster once you're under contract, giving you a real cushion against the clock.

Communicating proactively with both your lender and your real estate agent throughout this process is not optional. It's how you stay ahead of delays instead of reacting to them.

Negotiating and optimizing mortgage contingency terms

Once you understand mortgage contingency's logistics, optimizing terms in negotiation can maximize your protection and deal success.

Buyers and sellers can negotiate the length and details of mortgage contingency clauses. This means you're not stuck with whatever the listing agent's standard contract says. Everything is on the table.

Here's how to negotiate smarter:

- Shorten the window strategically: In a seller's market, offering a 21-day contingency instead of 30 makes your offer more attractive, but only if your lender can realistically close in that time

- Get pre-underwritten, not just pre-approved: A full underwriting review before you make an offer gives your lender a massive head start

- Specify your loan type clearly: Vague contingency language creates disputes; be precise about the loan type and amount

- Add a rate cap that's realistic: Don't put a cap so low it triggers automatically if rates shift slightly

- Negotiate extension rights: Ask for a built-in 5 to 10 day extension clause if you're in a market where appraisals run slow

Tips for getting the best contingency terms when buying or refinancing include working with a broker who knows what local sellers expect and can match your contingency terms to current market norms.

In slower markets, you have leverage. Push for longer contingency windows and stronger protections. In a hot seller's market, you might need to compress timelines while leaning heavily on your lender's speed.

Pro Tip: Consult your mortgage broker before finalizing contingency terms. A broker who understands mortgage origination strategies can advise you on realistic timelines and help you craft terms that protect you without scaring off the seller.

Our perspective: Why mortgage contingency is your real safety net

Here's what we've seen time and again: buyers get excited about winning a competitive offer and agree to waive their mortgage contingency to seal the deal. They think their pre-approval is iron-clad. It's not.

Pre-approvals are not loan approvals. They're estimates based on information you provided upfront. Once the property goes through underwriting, new issues can surface. Appraisals come in low. Employment is re-verified. Debt ratios shift. Any one of these can sink an approval.

Ignoring mortgage contingency is a leading cause of buyer deposit losses in U.S. real estate. We've watched buyers lose five-figure deposits because they were told contingency would kill their offer. Sometimes it's true. But losing $20,000 is far worse than losing a bidding war.

Our view is that contingency clauses deserve the same attention as the purchase price itself. They're not fine print. They're your financial lifeline. And with the right lender and the right preparation, you can offer a competitive timeline without sacrificing protection. The key is knowing what you're giving up before you agree to give it up. That clarity comes from working with someone who genuinely understands navigating compliance in mortgages and can walk you through the risk before you sign.

Explore your mortgage options with LoFi Rate

Understanding mortgage contingency is step one. Finding the right financing to satisfy it is step two, and that's where most buyers need the most help.

LoFi Rate connects you with licensed wholesale mortgage brokers who shop multiple lenders to find competitive rates, not just one bank's pricing. Whether you're navigating a tight contingency window or trying to lock in the best terms before closing, our mortgage broker matching process gives you access to options retail lenders simply don't offer. Explore our loan options at LoFi Rate and request a no-obligation consultation with a broker in your state today. You've worked hard to get your offer accepted. Let us help you protect it.

Frequently asked questions

What exactly does a mortgage contingency clause protect?

A mortgage contingency clause allows buyers to recover their earnest money deposit if they cannot secure financing within the agreed timeline. It's your legal right to exit the contract without financial penalty when the lender says no, as confirmed by mortgage compliance guidelines.

Can sellers refuse mortgage contingencies?

Sellers can reject mortgage contingencies, but most accept them to attract a larger pool of qualified buyers. In highly competitive markets, sellers may request buyers waive them, though contingency terms are negotiable between both parties.

What happens if you miss the mortgage contingency deadline?

Missing the deadline means you lose your contingency protection, which can lead to deposit forfeiture and contract cancellation. Staying ahead of your lender's timeline is critical, as strict deadlines apply once both parties sign.

How can buyers make their mortgage contingency more competitive?

Buyers can shorten their contingency window, obtain a fully underwritten pre-approval, and be specific about loan terms to show sellers they're serious. Working with the right lender matters too, and best contingency terms come from preparation, not luck.