TL;DR:

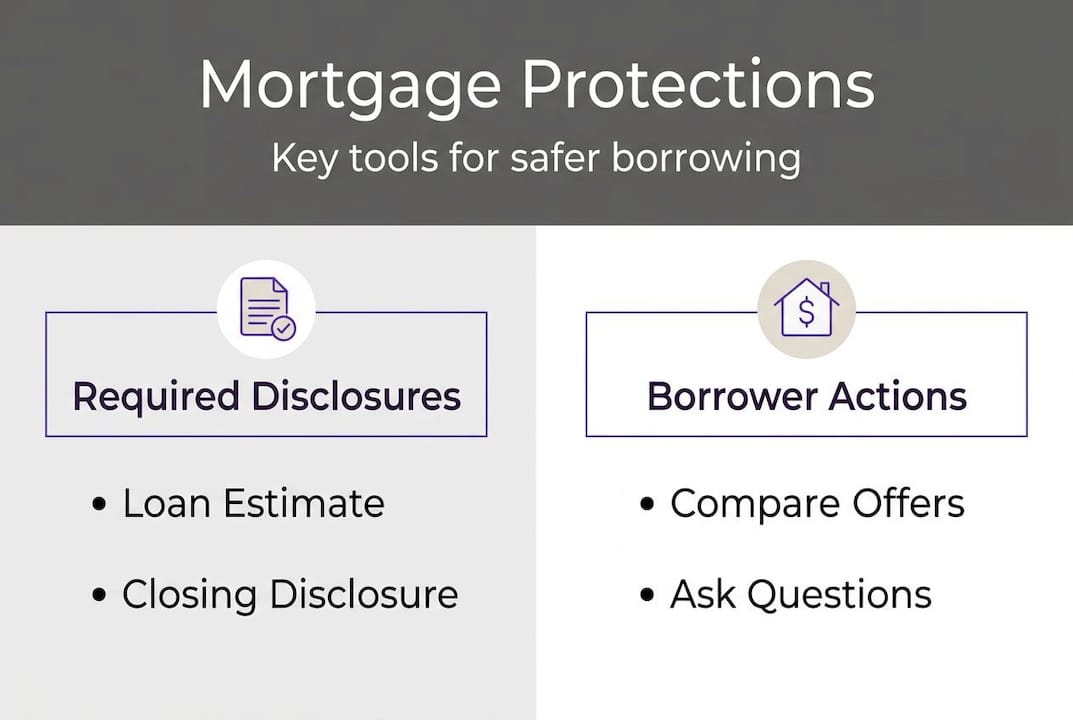

- Federal laws like TILA require lenders to provide standardized disclosures for better comparison.

- Both wholesale and retail mortgage channels are protected by the same federal rules but differ in competition and transparency.

- Borrowers should actively review documents, compare offers, and verify verbal promises to fully utilize protections.

Most homebuyers focus on the interest rate and the monthly payment. Few stop to ask: what laws are actually protecting me during this process? Federal mortgage consumer protections have been on the books for decades, yet many borrowers sign loan agreements without fully understanding what safeguards exist or where the gaps are. Choosing between a wholesale mortgage broker and a retail lender adds another layer of complexity. This guide cuts through the confusion, explains the key protections that apply to every borrower, and shows you how to use them whether you go the wholesale or retail route.

Table of Contents

- What is consumer protection in mortgages?

- Key consumer protections for mortgage borrowers

- Wholesale vs. retail mortgages: How protections apply and what's different

- How to use consumer protections to your advantage

- A better defense: What most mortgage guides miss about protecting yourself

- Get the best rates and full transparency with LoFiRate

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Standardized disclosures | Regulations require lenders to provide clear, comparable cost and term documents before you sign. |

| Protection for all buyers | Whichever mortgage route you choose—wholesale or retail—core consumer protections still apply. |

| Watch for steering and scams | Safeguards matter most when comparing lenders and closing your loan, so stay proactive and alert to red flags. |

| Actionable steps matter | Using your legal rights helps you get better rates and avoid costly surprises during the homebuying process. |

What is consumer protection in mortgages?

At its core, mortgage consumer protection is about leveling the playing field. Lenders and brokers work with mortgage products every single day. You probably do not. That gap in knowledge creates real risk for borrowers, who may not recognize a bad deal, hidden fees, or misleading terms without some help from the law.

Federal rules step in to reduce that gap. The Truth in Lending Act, commonly known as TILA, is the legal backbone of mortgage consumer protection. TILA requires lenders to give you standardized disclosures showing the annual percentage rate (APR), the total finance charge, and other key costs in a consistent format so you can actually compare offers side by side.

But consumer protection goes beyond disclosure. Here are the main protections that apply to most mortgage borrowers:

- Standardized disclosures: Every lender must show you the APR, finance charge, and total loan cost in the same format, making comparison shopping far more straightforward.

- Ability-to-repay rules: Lenders must verify your income, assets, and credit before approving a loan, reducing the risk of borrowers being approved for loans they cannot afford.

- Anti-steering rules: Brokers cannot push you toward a more expensive loan just because it pays them a higher commission.

- Rescission rights: For certain home-secured loans, federal law gives you three business days to cancel after signing, with no penalty.

The real goal of these rules is simple: reduce information asymmetry so that borrowers can make informed decisions rather than trusting claims they cannot verify.

You can also use the CFPB's homebuyer tools to explore rate comparisons, understand loan estimates, and learn how fees are calculated before you ever sit down with a lender.

Understanding mortgage compliance basics will also help you recognize when something feels off. Lenders who resist showing you detailed cost breakdowns or who rush you past disclosures are not just being unhelpful. They may be violating the very rules designed to protect you. Learning about navigating mortgage compliance gives you the language to push back confidently.

With the basics set, let's explore the specific protections you can expect and what they mean in practical terms.

Key consumer protections for mortgage borrowers

Protections do not just exist on paper. They show up at specific moments throughout your mortgage journey, from the first call with a lender to the day you sign at the closing table. Knowing when to expect them makes you a far more effective borrower.

Here is how these protections typically appear step by step:

- Shopping phase: When you request a quote, the lender or broker must provide a Loan Estimate within three business days. This document shows your rate, monthly payment, closing costs, and total loan cost in a standardized format.

- Comparison stage: Because every Loan Estimate follows the same layout, you can place two or three offers side by side and spot real differences in cost. This is exactly what the official disclosure guides are designed to help you do.

- Pre-approval and underwriting: Ability-to-repay rules require your lender to document your income and verify that you can realistically handle the loan. This protects you from approval for something unaffordable.

- Broker interactions: Anti-steering rules mean your broker cannot legally steer you toward a higher-cost product for their own financial gain. If a broker cannot explain why one option is better for you, that is a red flag worth pursuing.

- Closing week: Consumer protections around the closing process include scam prevention guidance. Wire fraud targeting homebuyers at closing is a growing crime. Verify wire instructions by phone using a number you found independently, never one from an email.

Using a mortgage shopping checklist can help you track disclosures and make sure no step gets skipped. Pairing that with a solid understanding of mortgage rate transparency means you will know exactly what numbers to question.

Pro Tip: Request your Loan Estimate in writing before you pay any fees. Federal rules require lenders to honor the terms on that document, giving you real leverage during negotiations.

Understanding those legal underpinnings, let's see how these protections show up when you compare your mortgage channel options.

Wholesale vs. retail mortgages: How protections apply and what's different

The mortgage market offers two main paths: wholesale and retail. Both are governed by the same federal disclosure rules, but the experience and potential risks differ in ways that matter.

| Feature | Wholesale (Broker) | Retail (Direct Lender) |

|---|---|---|

| Who you work with | Licensed mortgage broker | Lender's own loan officer |

| Lender options | Multiple wholesale lenders | One lender only |

| Rate competition | Higher, brokers shop around | Limited to that lender's pricing |

| Disclosure requirements | Same federal rules apply | Same federal rules apply |

| Main risk | Steering toward higher commissions | Missing better rates elsewhere |

| Transparency | Broker compensation disclosed | Internal pricing less visible |

Wholesale brokers work with a network of lenders and can submit your application to several at once. That competition can drive down your rate. The wholesale lender shopping guide explains how this process works in detail, and research consistently shows that broker access to competitive mortgage rates can produce meaningful savings over the life of a loan.

Retail lenders offer simplicity. You deal with one company, one process, one set of products. But simplicity has a cost. Without competing offers on the table, you have no way to know if you are getting a fair deal.

The wholesale-versus-retail structure changes how much competition you access, but federal protections still apply in both cases. Risks in wholesale tend to show up as potential steering or conflicts of interest. Risks in retail tend to show up as missed savings from not shopping around.

Pro Tip: Even if you prefer the simplicity of a retail lender, get at least one wholesale broker quote first. The comparison gives you real data to evaluate, not just a gut feeling.

Exploring mortgage competition insights and mortgage origination basics will help you understand exactly how each channel affects your bottom line.

Now that you know how wholesale and retail options compare, here is how you can turn protections into practical leverage.

How to use consumer protections to your advantage

Knowing protections exist is one thing. Actively using them is another. Borrowers who treat disclosures as checklists and ask pointed questions consistently get better outcomes than those who trust the process without verifying it.

Here are the steps that give you the most leverage:

- Request disclosures early: Ask for a Loan Estimate before you commit to anything. Federal rules require it within three business days, but you can ask for it sooner. Lenders who delay are worth questioning.

- Compare apples to apples: Line up Loan Estimates from multiple lenders. The standardized format exists specifically so you can do this without needing a finance degree.

- Verify verbal promises in writing: If a loan officer says your rate will be 6.5%, make sure that number appears in your written disclosure. Verbal terms mean nothing at closing.

- Watch for steering red flags: Vague explanations of fees, resistance to answering cost questions, or pressure to decide quickly are warning signs. Mechanics borrowers should focus on include demanding standardized disclosures early and verifying intended loan terms against documents before locking.

- Guard your closing funds: Wire fraud is real. Confirm transfer instructions by phone with your title company before sending any money.

- Keep copies of everything: Retain every disclosure, every Loan Estimate, and every Closing Disclosure. If a dispute arises, your paper trail is your protection.

Here is a quick reference for the documents you should have at each stage:

| Stage | Document to request | What to check |

|---|---|---|

| Shopping | Loan Estimate | APR, closing costs, monthly payment |

| Pre-closing | Closing Disclosure | Final rate, fees, cash to close |

| Closing | Signed copies of all docs | Terms match your Loan Estimate |

| Post-closing | Right of rescission notice | Applies to certain refinances |

Using a mortgage shopping checklist alongside resources on qualifying for a mortgage puts you in a position to ask the right questions at every stage. If something feels off during closing week, the CFPB scam prevention resources give you clear next steps.

A better defense: What most mortgage guides miss about protecting yourself

Most guides explain what consumer protection rules require. Far fewer tell you how to actually enforce them. That is the gap where borrowers get hurt.

Here is the uncomfortable truth: paperwork does not protect you. Reading the paperwork does. Borrowers who challenge inconsistencies, ask for written confirmation of verbal terms, and push back when explanations are vague consistently get better deals and fewer surprises. Those who assume the documents are correct because they were handed them by a professional often discover the mistake after signing.

The red flags are usually visible before closing. Vague cost explanations, resistance when you ask for documents, and inconsistency between what you were told on the phone and what appears in writing are all signs that something is not right. Understanding mortgage rate transparency helps you recognize those patterns quickly.

Protections are tools, not guarantees. You have to pick them up and use them.

Get the best rates and full transparency with LoFiRate

Armed with these insights, take the next step toward a protected, empowered mortgage experience. Consumer protections give you the framework, but finding the right lender through the right channel is what turns that framework into real savings.

LoFiRate connects you with licensed wholesale mortgage brokers who are required to shop multiple lenders on your behalf, giving you access to competitive rates that retail lenders simply cannot match by design. Every connection through LoFiRate's broker matching is built around transparency and compliance, so you get the full picture before you commit. Browse loan options tailored to your situation, or visit LoFiRate to request a no-obligation consultation and see what wholesale access can do for your rate.

Frequently asked questions

What are the main consumer protection laws for mortgages?

The Truth in Lending Act (TILA) is the primary federal law, requiring standardized disclosures and protections like ability-to-repay rules, anti-steering requirements, and rescission rights for eligible home-secured loans.

How do I know if my mortgage broker is acting in my best interest?

Ask for a Loan Estimate early, compare multiple offers, and make sure written terms match what you were told verbally. Steering and unclear cost explanations are the most common warning signs that a broker may not be working in your favor.

Are wholesale mortgages safer than retail from a consumer protection standpoint?

Federal disclosures protect buyers in both channels, but wholesale-versus-retail structure mainly changes who you interact with and how much lender competition you access. Wholesale offers more choice; retail offers simplicity with less comparison pressure.

What should I do if my closing costs or terms change at the last minute?

Treat any last-minute change as a red flag. CFPB guidance advises homebuyers to review disclosures carefully, ask direct questions, and contact consumer protection agencies if something feels wrong before you sign.